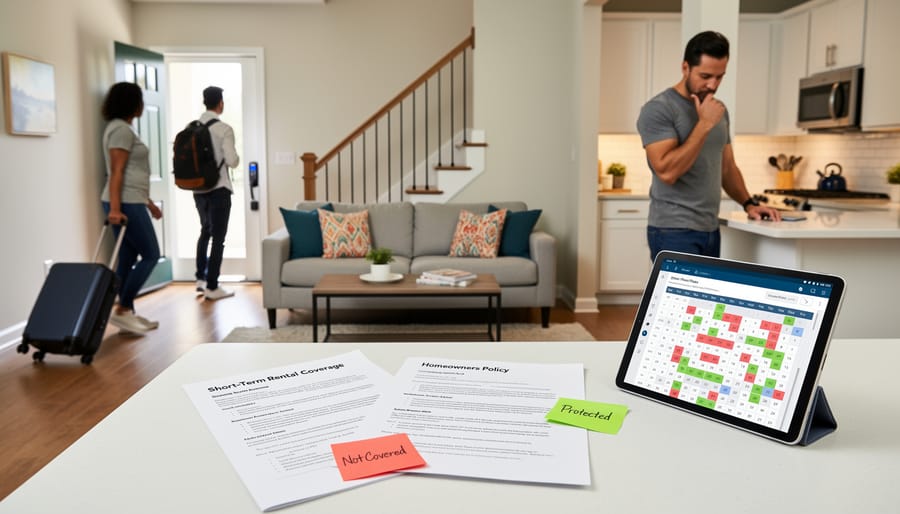

Your traditional homeowners insurance policy explicitly excludes coverage the moment you accept your first short-term rental booking. This gap leaves you personally liable for guest injuries, property damage, and lost income—exposures that can easily reach six figures from a single incident.

The financial stakes are considerable: A guest’s slip-and-fall lawsuit averages $50,000 in settlements, while a kitchen fire during occupancy can trigger $200,000+ in combined property damage and liability claims. Your standard policy won’t cover any of it because commercial activity voids residential coverage. Yet most property investors discover this only after filing a claim that gets denied.

Short-term rental insurance operates fundamentally differently from homeowners policies. It accounts for rotating occupants, commercial liability exposure, higher property damage frequency, and income replacement when your property becomes uninhabitable. You’re not just protecting a home—you’re insuring a revenue-generating business asset that faces unique risks every time new guests check in.

Three coverage pathways exist: endorsements added to existing policies (limited and increasingly rare), specialized STR policies from niche insurers, or comprehensive commercial dwelling policies with STR provisions. Each offers different protection levels, premium structures, and claim handling processes. The right choice depends on your rental frequency, property value, location, and risk tolerance.

This insurance category has evolved rapidly as platforms like Airbnb and VRBO transformed the hospitality landscape. Coverage that didn’t exist a decade ago is now essential for protecting your investment returns and personal assets. Understanding what you actually need—beyond the minimal host protection programs platforms provide—determines whether your short-term rental becomes a profitable investment or an expensive liability.

The Coverage Gap: Where Traditional Insurance Fails Short-Term Rentals

What Your Current Policy Actually Covers (Hint: Not Much)

Here’s the uncomfortable truth: your standard homeowners insurance policy was designed for one family living in one home—not a revolving door of vacationing strangers. Most traditional policies contain what’s called a “business activity exclusion” that automatically voids coverage the moment you start accepting paying guests, even if it’s just a weekend rental.

Think your policy covers you because you’re only renting occasionally? Think again. Insurance companies don’t distinguish between hosting once a month or 365 days a year. The second you list your property on Airbnb or VRBO, you’ve crossed into commercial territory. That means liability claims from guest injuries, property damage from parties gone wrong, or theft by guests could leave you completely exposed.

Standard policies also cap coverage at dangerously low levels for short-term rental scenarios. While your homeowners policy might cover vandalism from a break-in, it likely won’t cover a guest who trashes your place during a three-day stay. The frequent turnover inherent to short-term rentals dramatically increases risk exposure—something traditional insurers simply won’t accommodate.

Even more concerning is the liability gap. If a guest slips on your stairs or gets food poisoning from your fully-equipped kitchen, your personal liability coverage may deny the claim entirely since the injury occurred during a commercial activity. We’re talking potential out-of-pocket expenses reaching six figures or more, depending on the severity of injuries and your state’s liability laws.

The Costly Mistakes Property Owners Make

Many property owners discover costly insurance coverage gaps only after filing a claim. The most common misconception? Believing their standard homeowners policy covers short-term rental activity. It doesn’t.

Consider Sarah, a Toronto homeowner who listed her basement suite on Airbnb to offset her mortgage. When a guest slipped on her icy driveway and sued for $150,000, her insurer denied the claim entirely. Her homeowners policy explicitly excluded commercial activity, leaving her personally liable for medical expenses and legal fees.

Another expensive mistake involves assuming business liability coverage extends to property damage. Mark, a Vancouver investor, learned this the hard way when guests threw an unauthorized party that caused $35,000 in damage. While his policy covered the liability claims from injured partygoers, it didn’t cover the trashed interior, broken appliances, or stolen electronics.

The assumption that platform-provided coverage is comprehensive also trips up many hosts. Airbnb’s Host Guarantee has notable exclusions: cash, securities, collectibles, and certain personal property items aren’t covered. One cottage owner discovered this after guests damaged a $12,000 antique dining set, receiving nothing from the platform’s protection program.

Perhaps the costliest oversight is underinsuring for loss of income. When properties require repairs after guest damage, owners without proper business interruption coverage lose both rental income and still owe their mortgage, creating a devastating financial squeeze that can last months.

Types of Insurance Your Short-Term Rental Actually Needs

Short-Term Rental Property Insurance

Traditional homeowners insurance simply wasn’t designed for the unique risks of running a short-term rental business, which is where specialized STR policies come in. These purpose-built policies acknowledge that your property isn’t just a home—it’s a revenue-generating asset that faces different exposures than a standard residence.

A comprehensive STR policy typically includes three core components. First, dwelling protection covers your physical structure and attached fixtures against common perils like fire, wind, and vandalism. Unlike standard policies that might deny claims when they discover rental activity, STR insurance explicitly covers damage occurring during guest stays. This means you’re protected whether the property sits vacant, you’re using it personally, or guests are checked in.

Second, liability coverage is crucial since you’re regularly inviting strangers onto your property. If a guest slips on your stairs or suffers carbon monoxide poisoning, you could face substantial legal claims. STR policies provide liability limits starting around $1 million, with options to increase coverage through umbrella policies.

Third, and perhaps most valuable for investors, is loss of income coverage. This replaces rental revenue when your property becomes uninhabitable due to a covered event. If a kitchen fire forces you to cancel bookings during peak season, this coverage ensures your mortgage still gets paid. Some policies even cover cancellations due to specific scenarios like mandatory evacuations or utility failures—critical protections that standard homeowners policies completely exclude.

Commercial Liability Coverage: Your First Line of Defense

Commercial liability coverage serves as your financial safety net when guests are on your property. If a visitor slips on your deck, gets injured in your hot tub, or claims they suffered food poisoning from your kitchen appliances, this coverage steps in to handle medical expenses and legal costs. Without it, you’re personally exposed to lawsuits that could easily exceed six figures.

The risk profile for short-term rentals differs significantly from traditional long-term tenancies. You’re hosting a rotating door of strangers who aren’t familiar with your property’s quirks, increasing the likelihood of accidents. Additionally, guest property damage claims, like a broken laptop from a ceiling leak or ruined belongings from a fire, fall under this umbrella.

Most insurance advisors recommend minimum liability limits of $1 million for short-term rental properties, though $2 million provides more robust protection if you’re in a litigious area or operate a luxury property. The sweet spot typically ranges between $1-2 million for standard vacation rentals. Properties with pools, hot tubs, or other amenity-rich features warrant higher limits due to elevated risk exposure.

Consider this your foundational layer before exploring additional specialized coverages. While it might seem like an unnecessary expense when nothing’s gone wrong, one serious injury claim could potentially wipe out years of rental income and jeopardize your entire investment portfolio.

Loss of Income Protection

Loss of income protection, sometimes called business interruption coverage, safeguards your rental revenue when covered perils make your property temporarily uninhabitable. Unlike traditional homeowners policies that ignore lost rental income, this coverage bridges the financial gap between property damage and full restoration.

Here’s how it works in practice: Say your short-term rental generates $3,500 monthly through steady bookings. A kitchen fire forces you to cancel reservations for two months while repairs are completed. Loss of income protection would compensate you for that $7,000 in missed revenue, minus your deductible.

The calculation typically multiplies your average nightly rate by the number of days your property remains unrentable. If you charge $200 per night with 80% occupancy and repairs take 45 days, you’d recover approximately $7,200 (200 x 45 x 0.80). Most policies base this on your documented booking history from platforms like Airbnb or Vrbo, making accurate record-keeping essential.

Coverage limits usually range from three to twelve months of lost income, with premiums reflecting your property’s revenue potential. Consider choosing a limit that matches your area’s typical repair timeline. In markets where contractor availability is limited, opt for longer coverage periods. This protection essentially functions as a cash flow safety net, ensuring your investment property continues generating returns even when guests can’t check in.

Platform-Provided Coverage: What Airbnb and VRBO Really Protect

Airbnb Host Guarantee vs. Host Protection Insurance

Airbnb offers two distinct protection programs that hosts often confuse or assume provide comprehensive coverage—they don’t. Understanding the differences is crucial before you find yourself facing an uncovered loss.

The Host Guarantee provides up to $3 million in property damage protection caused by guests. It covers damage to your dwelling, detached structures, and personal property. However, here’s the catch: it excludes cash, securities, collectibles, pets, and common carrier liability. More importantly, it only kicks in after your personal insurance, operates on an actual cash value basis (not replacement cost), and requires extensive documentation that many hosts struggle to provide during effective claims management.

Host Protection Insurance offers $1 million in liability coverage if a guest or another third party gets injured during their stay. It protects you against bodily injury claims and property damage caused to others. Notable exclusions include motor vehicles, watercraft, intentional acts, and certain animals. This coverage also won’t protect you from liability arising from co-host activities or issues with neighboring properties.

The claim process for both programs presents significant challenges. Airbnb requires proof that standard insurance won’t cover the incident, detailed photographic evidence before repairs, and often denies claims for pre-existing conditions that hosts didn’t document. Response times frequently exceed 30 days, and many hosts report lowball settlement offers based on depreciated values rather than replacement costs.

Neither program replaces dedicated short-term rental insurance. They’re secondary coverage at best, leaving substantial gaps that could jeopardize your investment property returns.

VRBO’s $1 Million Liability Insurance: The Fine Print

VRBO’s $1 million liability insurance sounds impressive on paper, but understanding what it actually covers is essential for protecting your investment property. This platform-provided coverage, underwritten by Lloyd’s of London, activates only when a verified guest causes bodily injury or property damage to a third party during their stay.

Here’s the critical distinction: VRBO’s liability insurance protects you from claims made by others against your guests, not from damage your guests cause to your property. For example, if a guest’s cooking fire spreads to neighboring units, you’re covered. However, if that same guest burns your kitchen countertops, you’re not.

The coverage comes with significant exclusions that create concerning gaps. It doesn’t protect against claims related to sexual misconduct, assault, communicable diseases, or intentional acts. Properties with certain amenities like trampolines, tree houses, or some pool configurations may find coverage limited or excluded entirely. Additionally, the policy only covers incidents during active, paid reservations booked through VRBO’s platform.

Perhaps most importantly, this coverage doesn’t replace the commercial liability insurance lenders typically require for investment properties. It’s supplemental protection, not primary coverage. Many property owners discover too late that VRBO’s insurance won’t satisfy their mortgage requirements or adequately protect their assets.

Smart property investors treat VRBO’s coverage as a backup layer, not their main defense. To properly protect your short-term rental investment, you’ll need dedicated commercial liability insurance with higher limits, broader coverage, and protections specifically designed for vacation rental operations.

How Much Does Short-Term Rental Insurance Actually Cost?

Factors That Impact Your Premium

Understanding what drives your premium helps you make smarter coverage decisions and potentially save money. Insurance carriers evaluate several key factors when pricing short-term rental policies.

Location ranks among the most significant variables. Properties in coastal areas prone to hurricanes, regions with wildfire risks, or neighborhoods with higher crime rates typically command steeper premiums. Your ZIP code alone can swing costs by hundreds of dollars annually.

Property type and age also matter considerably. A vintage Victorian requires more coverage than a newer construction due to aging systems and potential code compliance issues. Multi-unit properties naturally cost more to insure than single-family homes.

Rental frequency directly impacts your risk profile. A property booked 200 nights yearly faces greater exposure than one rented occasionally, which insurers price accordingly. Some carriers offer tiered pricing based on occupancy rates.

Your claims history follows you. Previous liability claims or property damage on any rental property can increase premiums by 20-40 percent, even with a new insurer.

Safety features work in your favor. Installing monitored security systems, smart locks, fire suppression equipment, and impact-resistant roofing can earn meaningful discounts. Many insurers now offer credits for professional property management oversight, recognizing the reduced risk that comes with experienced operators handling guest screening and property maintenance.

Smart Ways to Lower Your Insurance Costs

Reducing your short-term rental insurance premiums doesn’t mean sacrificing protection. Start by investing in comprehensive security systems, including smart locks, surveillance cameras, and smoke detectors. Most insurers offer significant discounts for properties with enhanced security features, sometimes reducing premiums by 10-20%. These systems also protect your investment by deterring problematic guests and providing evidence if claims arise.

Implement rigorous guest screening procedures through your booking platform. Requiring verified IDs, minimum stay requirements, and security deposits signals to insurers that you’re managing risk proactively. Some carriers even offer lower rates for hosts who maintain high guest ratings and thorough vetting processes.

Consider increasing your deductible if you have adequate cash reserves. Moving from a $500 to $1,000 deductible can reduce your annual premium by 15-25%. This strategy works best for experienced hosts with stable operations who rarely file claims.

Bundling policies with one carrier typically unlocks multi-policy discounts. If you own multiple rental properties or carry other insurance types like auto or umbrella coverage, consolidating them with your short-term rental insurer can yield savings of 5-15%.

Finally, shop around annually. The short-term rental insurance market evolves rapidly, with new providers entering regularly. What’s competitive today may not be tomorrow’s best deal.

Finding the Right Insurance Provider for Your Rental Property

Questions Every STR Owner Must Ask Before Buying

Before signing any policy, arm yourself with these critical questions. Start with coverage specifics: Does the policy cover guest injuries, property damage caused by guests, and theft of your belongings? What’s the difference between actual cash value and replacement cost coverage for your furnishings? Understanding these distinctions can mean thousands of dollars in a claim situation.

Next, clarify the claims process. How quickly does the insurer respond to claims, and what documentation will you need? Ask about their track record with STR claims specifically, as some carriers are more familiar with this niche than others.

Don’t skip the exclusions conversation. Which scenarios aren’t covered? Many policies exclude damage from certain events or guest counts exceeding specific limits. Understanding these gaps now prevents nasty surprises later.

Finally, discuss policy flexibility. What happens if you switch from full-time STR to occasional rentals? Can your coverage adapt if you decide to accept long-term tenants instead? As your investment strategy evolves, your insurance should evolve with it. Request everything in writing and compare responses from multiple insurers before making your decision.

Specialized STR Insurers vs. Traditional Carriers

When choosing insurance for your short-term rental, you’ll face a key decision: specialized STR insurers or traditional carriers with endorsements. Each approach has distinct advantages worth considering.

Specialized STR insurers like Proper Insurance, CBIZ, and Safely offer policies specifically designed for platforms like Airbnb and VRBO. The major advantage? They inherently understand your business model. These providers typically offer streamlined coverage without extensive policy modifications, include commercial liability limits appropriate for guest injuries, and often provide faster claims processing since they’re familiar with STR-specific scenarios. You won’t need to explain what “turnover damage” means or why you need coverage for 50+ different guests annually.

However, specialized policies often come at a premium, sometimes costing 2-3 times more than traditional homeowners insurance. They may also require you to bundle multiple properties or commit to annual contracts.

Traditional carriers with STR endorsements present an alternative path. Adding a short-term rental rider to your existing homeowners policy keeps your insurance relationship consolidated and may cost less initially. This works particularly well if you’re renting occasionally rather than operating a full-time rental business.

The drawback? Traditional insurers may impose strict limitations on rental days, exclude certain coverage types, or struggle with claims unique to the STR industry. Your choice ultimately depends on rental frequency, property value, and risk tolerance.

Protecting Your Investment Beyond Insurance

While comprehensive insurance forms your financial safety net, savvy short-term rental operators know that preventing problems beats filing claims every time. Think of insurance as your backup plan—these proactive measures are your frontline defense.

Start with rigorous guest screening. Platforms like Airbnb and Vrbo offer basic verification, but consider requiring government-issued ID, reading past reviews carefully, and trusting your instincts when something feels off. Some hosts use third-party screening services that check criminal backgrounds and eviction histories, especially for longer bookings. Remember, declining a sketchy reservation costs nothing compared to property damage or liability issues.

Security deposits and damage waivers provide another layer of protection. While many hosts hesitate to require deposits fearing they’ll discourage bookings, platforms now offer damage protection programs that charge guests a non-refundable fee instead. This approach often works better than traditional deposits, which can trigger disputes and negative reviews.

Your rental agreement shouldn’t be an afterthought copied from the internet. A solid contract clearly outlines house rules, maximum occupancy, prohibited activities, and consequences for violations. It’s your legal foundation if disputes arise and demonstrates due diligence to your insurer.

Smart home technology has revolutionized property risk management strategies. Noise monitors alert you to parties without recording conversations. Smart locks eliminate key exchanges and let you remotely grant access. Water leak detectors can prevent catastrophic damage, while exterior cameras (disclosed to guests) deter misconduct and provide evidence if needed.

Finally, maintain an emergency preparedness plan. Stock first aid kits, fire extinguishers, and clear evacuation instructions. Establish relationships with local contractors for urgent repairs. Create a 24/7 guest communication protocol so problems get addressed immediately, not after they escalate.

These risk mitigation strategies work synergistically with your insurance coverage, reducing claim frequency while protecting your property’s condition and your peace of mind. Better yet, many insurers offer premium discounts when you demonstrate robust risk management practices.

Protecting your short-term rental property isn’t just about checking a box on your investment checklist—it’s about safeguarding the foundation of your income-generating asset. As we’ve explored throughout this guide, traditional homeowners insurance simply won’t cover the unique exposures that come with operating an STR business. From guest-related liability claims to business interruption coverage that protects your rental income, the right insurance strategy is as crucial to your success as choosing the right property location or implementing effective real estate investment strategies.

The good news? Specialized STR insurance has evolved significantly, with competitive options now available that specifically address the dual nature of your property as both a physical asset and an income stream. Whether you opt for a comprehensive short-term rental policy, enhance your homeowners coverage with appropriate endorsements, or layer commercial coverage onto your existing protection, the key is ensuring you have adequate coverage before—not after—a claim occurs.

Now is the time to take action. Review your current insurance policy with fresh eyes, armed with the knowledge you’ve gained here. Identify the coverage gaps specific to your rental operation, and don’t hesitate to reach out to insurance specialists who understand the STR landscape. The investment you make in proper coverage today could mean the difference between a minor setback and a catastrophic financial loss tomorrow. Your rental property deserves protection that works as hard as you do.