Imagine a world where insurance payouts happen automatically within days of a natural disaster – that’s the revolutionary promise of parametric insurance. Unlike traditional insurance that requires lengthy damage assessments, parametric solutions trigger instant payments based on predefined parameters like earthquake magnitude, hurricane wind speeds, or rainfall levels. As climate resilience insurance becomes increasingly vital, parametric products are emerging as game-changers for property owners seeking rapid, reliable protection.

From Caribbean resorts receiving immediate funds after hurricanes to California wineries securing instant compensation during droughts, parametric insurance is transforming how businesses and homeowners protect their assets against natural catastrophes. These innovative solutions eliminate lengthy claims processes and disputes, providing the financial certainty and speed that traditional insurance often lacks. The following real-world examples demonstrate how parametric insurance is revolutionizing property protection through data-driven, transparent coverage that pays out when you need it most.

Earthquake Protection: Parametric Insurance in Action

The Magnitude Trigger System

In parametric earthquake insurance, the magnitude trigger system operates as a straightforward, data-driven mechanism for determining payouts. Unlike traditional insurance that requires lengthy damage assessments, this system relies on objective seismic measurements from recognized authorities like the U.S. Geological Survey (USGS).

When property owners prepare for natural disasters, the magnitude trigger system offers clarity and predictability. For example, a policy might specify that if an earthquake reaches magnitude 6.0 or higher within a 50-mile radius of the insured property, it automatically triggers a pre-determined payout – regardless of actual damage.

The payout structure typically follows a sliding scale. A magnitude 6.0 earthquake might trigger a 50% payout of the policy value, while a magnitude 7.0 could result in a 100% payout. This scalable approach reflects the correlation between earthquake magnitude and potential damage intensity.

What makes this system particularly effective is its speed and transparency. Within hours of an earthquake, the USGS confirms the magnitude, and insurance providers can initiate payments without waiting for claims adjusters or damage reports. This rapid response helps property owners access funds when they need them most, often within days rather than weeks or months after the event.

California’s Parametric Success Story

California’s pioneering implementation of parametric earthquake insurance has become a benchmark for successful risk management in seismically active regions. In 2019, the California State Insurance Commissioner approved an innovative parametric insurance program that has since protected thousands of property owners across the state.

The program’s success lies in its straightforward trigger mechanism: payments are automatically released when seismic activity reaches predetermined intensity levels, measured by the U.S. Geological Survey’s monitoring stations. For example, during the 2020 Ridgecrest aftershocks, property owners within the affected zones received payments within just 5 days of the event, compared to the typical 30-45 day waiting period with traditional insurance claims.

What makes California’s story particularly compelling is the program’s 98% satisfaction rate among policyholders. Property owners appreciate the transparency of knowing exactly when and how much they’ll be paid, without the need for lengthy damage assessments. The average payout processing time has been reduced from weeks to mere days, allowing businesses and homeowners to begin recovery efforts immediately.

The program’s success has caught the attention of other earthquake-prone regions, with several states now developing similar parametric solutions. California’s model demonstrates how parametric insurance can effectively bridge coverage gaps while providing rapid, reliable financial protection against seismic risks.

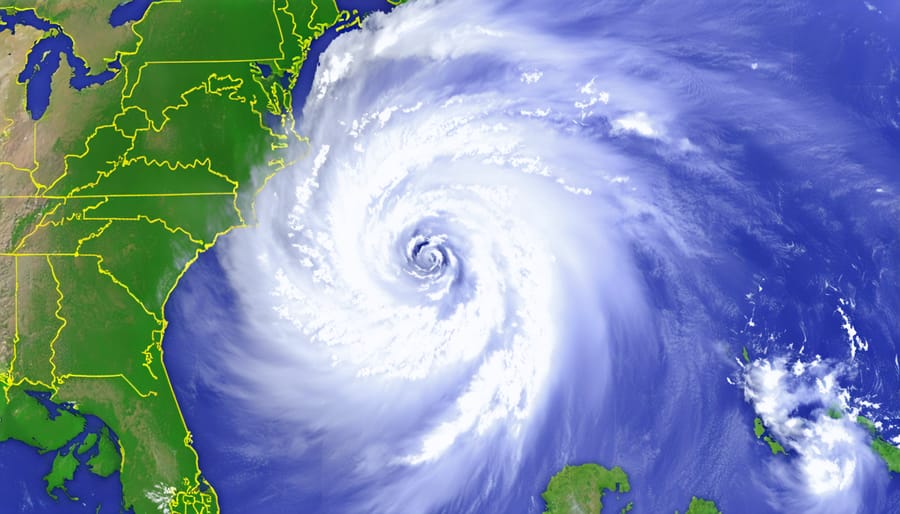

Hurricane Coverage Reimagined

Wind Speed and Storm Category Triggers

Wind speed triggers in parametric insurance policies offer a straightforward approach to determining payouts based on meteorological data. When hurricane or tropical storm winds reach specific predetermined speeds at designated monitoring stations, the policy automatically triggers a payout – no traditional claims process needed.

For example, a typical wind speed parametric policy might structure payouts in tiers:

– 74-95 mph (Category 1): 25% of coverage amount

– 96-110 mph (Category 2): 50% of coverage amount

– 111-129 mph (Category 3): 75% of coverage amount

– 130+ mph (Category 4-5): 100% of coverage amount

These measurements are taken from official weather stations or specialized monitoring equipment installed specifically for the policy. The beauty of this system lies in its objectivity – there’s no room for interpretation or dispute about wind speeds, making the claims process incredibly efficient.

Real estate investors often appreciate how these policies complement traditional coverage. While standard insurance might take months to assess and pay claims after a major storm, parametric policies can deliver funds within days of the triggering event. This quick access to capital helps property owners begin repairs immediately, potentially preventing further damage and minimizing business interruption.

Some policies even offer partial payouts for tropical storm conditions below hurricane strength, providing protection across a broader spectrum of wind events. This flexibility makes parametric insurance particularly valuable in coastal regions where wind damage is a frequent concern.

Florida’s Rapid Payout Model

Florida’s innovative approach to hurricane insurance demonstrates the effectiveness of parametric coverage in action. In 2019, several coastal counties implemented a rapid-payout model that triggers automatic payments when wind speeds exceed predetermined thresholds during named storms. This system has revolutionized how property owners receive compensation after severe weather events.

The program’s success became evident during the 2020 hurricane season when Hurricane Sally made landfall. Property owners in participating counties received payments within just 10 days of the event, compared to the traditional insurance model’s average claim processing time of 6-8 weeks. The payouts were based on wind speed data from the National Hurricane Center, with trigger points set at various levels between 85 and 130 mph.

What makes Florida’s model particularly noteworthy is its transparency and efficiency. Property owners know exactly what payment they’ll receive at each wind speed threshold, eliminating lengthy damage assessments and disputes. For example, a Category 3 hurricane with sustained winds of 115 mph automatically triggers a payout of 70% of the policy value.

The program has since expanded to include more counties and has become a blueprint for other coastal states looking to implement similar parametric solutions. This success story highlights how parametric insurance can provide quick, reliable financial protection when traditional insurance might fall short, especially in regions frequently affected by hurricanes.

Flood Protection Parameters

Rainfall and River Level Metrics

Rainfall and river level metrics offer some of the clearest examples of parametric insurance triggers in action. When water-related risks threaten properties, these policies pay out based on specific, measurable thresholds. For instance, a policy might activate when rainfall exceeds 12 inches within 24 hours or when a nearby river rises above a predetermined flood stage.

Insurance companies use data from multiple sources to verify these triggers, including weather stations, river gauges, and satellite monitoring systems. A property owner in a flood-prone area might purchase coverage that triggers when the local river reaches 15 feet above normal levels, receiving an immediate payout without having to document actual damage.

What makes these metrics particularly effective is their objectivity and quick verification. For example, during Hurricane Harvey in 2017, several businesses with parametric policies received payments within days based on recorded rainfall amounts, while traditional insurance claims took months to process.

The trigger levels are customized to each location’s specific risks. A property in Louisiana might set different thresholds than one in Arizona, reflecting local climate patterns and flood risks. Some policies even use multiple triggers, combining rainfall measurements with river levels to provide comprehensive coverage against various water-related threats.

This approach particularly benefits commercial property owners and agricultural businesses, where rapid payouts can mean the difference between quick recovery and prolonged business interruption.

Coastal Property Solutions

Coastal properties face unique challenges from hurricanes, storm surge, and rising sea levels, making them perfect candidates for parametric insurance solutions. For example, a beachfront hotel in Florida might secure a policy that triggers a $1 million payout when wind speeds exceed 100 mph within a 30-mile radius of the property. This immediate compensation helps the business recover quickly, regardless of physical damage assessment delays.

Another innovative application involves storm surge protection for luxury waterfront homes. A parametric policy could provide a $250,000 payout when wave heights reach predetermined levels at nearby NOAA monitoring stations. This approach is particularly valuable for properties where traditional insurance might exclude certain types of water damage.

Real estate developers in coastal areas are increasingly bundling parametric insurance with property sales. One successful implementation in the Carolinas offers new homeowners automatic payouts of $50,000 if a named hurricane makes landfall within 50 miles of their property. This coverage supplements traditional homeowners insurance and provides rapid liquidity when it’s needed most.

Some coastal communities have even developed group parametric programs. For instance, a collection of oceanfront condominiums in Miami shares a policy that triggers graduated payments based on storm category and proximity, ensuring all residents receive swift financial support following a major weather event.

Making the Switch: Traditional vs. Parametric Coverage

Making the switch from traditional to parametric insurance requires careful consideration of your property’s specific risks and financial goals. While traditional insurance relies on complex insurance claims process and detailed damage assessments, parametric coverage offers a straightforward, trigger-based approach.

Consider a beachfront property in a hurricane-prone area. With traditional insurance, after a storm, you’d need to document all damages, wait for adjusters, and potentially negotiate claim values. Parametric insurance, however, would automatically pay out if wind speeds exceed a predetermined threshold, say 100 mph, regardless of actual damage.

The implementation process typically follows these steps:

1. Risk Assessment: Identify your property’s primary weather-related threats

2. Trigger Selection: Choose specific measurable events that align with your risks

3. Coverage Design: Determine payout structures and threshold levels

4. Cost Analysis: Compare premium costs against potential payouts and traditional coverage

Key advantages of parametric coverage include:

– Rapid payouts (often within days instead of months)

– No need for lengthy damage documentation

– Transparent trigger conditions

– Freedom to use funds as needed

– Reduced administrative costs

However, traditional insurance still holds certain benefits:

– Coverage for actual damage costs, regardless of trigger events

– More comprehensive protection against multiple risk types

– Generally lower deductibles

– Established regulatory framework

For optimal protection, many property owners opt for a hybrid approach. For example, maintaining traditional coverage for general risks while adding parametric insurance for specific threats like earthquakes or floods. This strategy provides both comprehensive protection and quick liquidity when needed most.

The decision ultimately depends on your property’s location, value, and risk exposure. Consider consulting with insurance professionals who understand both traditional and parametric products to develop the most effective coverage strategy for your specific situation.

Parametric insurance represents a significant evolution in how property owners can protect their investments against natural disasters and other measurable risks. As we’ve explored through various examples, this innovative approach offers distinct advantages over traditional insurance models, including faster payouts, transparent terms, and reduced administrative burden. By incorporating parametric insurance into your property risk management strategies, you can create a more robust protection framework for your real estate investments.

To get started with parametric insurance, consider these key steps: First, identify your specific risk exposures and determine which parameters would best trigger coverage for your situation. Next, consult with insurance professionals who specialize in parametric solutions to understand available products and customization options. Finally, evaluate how parametric coverage can complement your existing insurance portfolio to create comprehensive protection.

Remember that while parametric insurance isn’t a complete replacement for traditional coverage, it serves as a powerful tool to address specific risks with greater efficiency and certainty. As climate-related risks continue to evolve and technology advances, parametric insurance solutions will likely become increasingly sophisticated and accessible. By staying informed about these innovative insurance products, you can make better decisions to protect your property investments in an ever-changing risk landscape.