Every time you pay your property insurance premium, a hidden cost lurks within that bill: medical billing fraud. This silent epidemic adds an estimated 10% to your insurance costs annually, whether you’re a homeowner, landlord, or real estate investor. Medical billing fraud occurs when healthcare providers, patients, or third parties deliberately submit false or inflated claims to insurance companies—and the financial ripple effects extend far beyond health insurance into the property and casualty coverage you depend on.

Understanding Insurance Fraud Prevention and Detection becomes crucial when you realize that fraudulent medical claims filed after slip-and-fall incidents on your property, or exaggerated injuries from minor accidents, directly impact your liability premiums. Insurance companies spread these losses across all policyholders, meaning you absorb costs for crimes you didn’t commit.

The schemes vary in sophistication. A contractor might bill for physical therapy sessions never attended after a workplace injury on your renovation project. A tenant could conspire with a dishonest chiropractor to inflate treatment costs following a legitimate accident. Medical providers sometimes engage in upcoding, billing for expensive procedures when simpler treatments were administered, or unbundling services to maximize reimbursements.

For real estate professionals and property owners, the stakes extend beyond premium increases. A pattern of questionable medical claims tied to your properties can trigger coverage denials, policy non-renewals, or difficulty securing affordable insurance in competitive markets. This financial vulnerability makes understanding medical billing fraud not just an abstract concern, but a practical necessity for protecting your property investments and maintaining sustainable insurance costs.

What Medical Billing Fraud Actually Looks Like

The Most Common Schemes Targeting Property Owners

Property owners face unique vulnerabilities when it comes to medical billing fraud. Understanding these common schemes can help you protect both your assets and your insurance premiums.

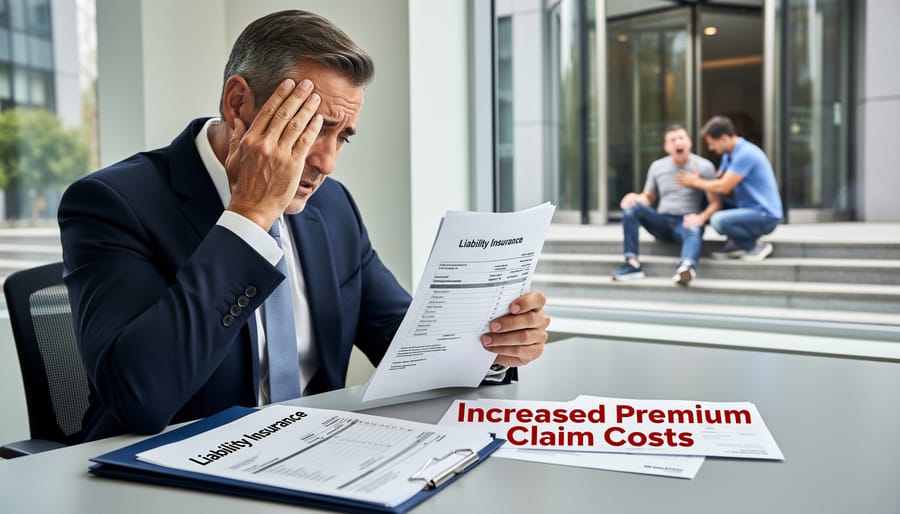

Slip-and-fall fraud remains one of the most prevalent schemes targeting homeowners. Professional scammers identify properties with perceived hazards—cracked sidewalks, uneven steps, or icy walkways—then deliberately fall and claim injury. What makes this particularly insidious is the collaboration with unethical medical providers who inflate treatment costs or bill for unnecessary procedures. A simple claimed ankle sprain can quickly balloon into tens of thousands of dollars in fraudulent medical bills submitted to your homeowner’s insurance.

Staged accidents at rental properties present another significant threat. Fraudsters may target landlords and property managers by orchestrating incidents in common areas, then seeking excessive medical treatments. These schemes often involve multiple participants who share in the settlement payouts.

Contractor-related medical fraud deserves special attention from real estate professionals. In this scenario, contractors or their employees claim work-related injuries on your property, then submit inflated medical bills or bills for treatments never received. Some even claim pre-existing conditions occurred on-site. Because property owners carry liability insurance, they become prime targets for these elaborate schemes.

The financial impact extends beyond individual claims. Each fraudulent incident contributes to rising insurance premiums across the real estate sector. Property investors and homeowners ultimately bear these costs through higher policy rates, making fraud prevention not just a personal concern but an industry-wide imperative.

Red Flags You Can Spot on Your Own Bills

Reviewing your medical bills doesn’t require a degree in healthcare administration. Start by checking for duplicate charges—the same procedure listed twice on the same date is a major red flag. Look for services you never received, like physical therapy sessions you didn’t attend or lab tests your doctor never ordered. Pay attention to dates; if a bill shows treatments on days you weren’t even at the facility, something’s wrong.

Watch for “upcoding,” where a simple office visit mysteriously becomes a complex consultation with a much higher price tag. Generic medications billed as brand-name drugs are another common trick. Check quantities too—did you really receive 30 bandages during a routine checkup?

Timing matters as well. Claims filed months after your visit, especially for services typically billed immediately, deserve scrutiny. Be wary of unbundled charges, where procedures normally billed together appear as separate line items to inflate costs. These fraudulent practices don’t just affect your out-of-pocket expenses; they drive up insurance premiums across the board, including the liability coverage crucial to property investments. When insurance companies pay inflated medical claims from slip-and-fall incidents on your rental properties, those costs eventually circle back to you through higher premiums.

Why This Matters for Your Property Insurance and Bottom Line

Medical billing fraud might seem like a healthcare-only concern, but it creates a ripple effect that directly impacts your property-related expenses and investment decisions. When fraudulent medical claims inflate the overall cost of insurance across the board, property owners and real estate investors feel the pinch in their wallets.

Here’s the connection: liability insurance for rental properties, slip-and-fall coverage for commercial buildings, and even homeowner policies all fall under the broader insurance ecosystem. When medical billing fraud drives up healthcare-related claims by an estimated $68 billion annually in the United States alone, insurers compensate by raising rates across multiple product lines. This means your insurance premiums for property coverage increase even when you’ve never filed a claim.

For landlords, the stakes are particularly high. Property liability insurance protects you when tenants or visitors suffer injuries on your premises. Fraudulent injury claims, often accompanied by inflated medical bills, can cost landlords thousands in increased premiums. Industry data suggests that fraudulent claims account for approximately 10 percent of total property and casualty insurance losses, translating to roughly $30 billion in extra costs passed along to policyholders.

Real estate investors making property acquisition decisions must factor these rising insurance costs into their calculations. A multi-unit residential property that seemed profitable on paper can quickly become marginal when annual insurance costs jump 15 to 25 percent due to fraud-driven rate increases. Commercial property owners face similar challenges, with general liability premiums climbing steadily as medical fraud inflates the cost of settling injury claims.

The bottom line is straightforward: every fraudulent medical bill that gets paid contributes to higher insurance costs for property owners. Understanding this connection helps you advocate for fraud prevention measures, scrutinize claims more carefully, and make more informed decisions about property insurance coverage levels and deductible structures that protect your investment returns.

How Insurance Companies Actually Detect Fraud

Technology Revolutionizing Fraud Detection

The insurance industry has entered a new era of fraud prevention, powered by sophisticated technology that’s making it increasingly difficult for fraudsters to game the system. Artificial intelligence and machine learning algorithms now analyze millions of billing records in seconds, identifying patterns and anomalies that human auditors might miss. These systems learn from historical fraud cases, becoming smarter over time at spotting red flags like duplicate claims, unusual billing codes, or treatment patterns that don’t align with diagnoses.

Automated billing audits have become particularly effective at catching medical billing fraud before claims get paid. These systems cross-reference treatment codes, compare costs against regional averages, and flag inconsistencies in provider billing histories. For instance, if a medical provider suddenly starts billing for significantly more expensive procedures or submitting unusually high claim volumes, the system triggers an immediate review.

What does this mean for you as a property owner or real estate professional? These technological safeguards help keep your insurance premiums more stable by reducing the losses insurance companies absorb from fraudulent claims. When insurers pay out less in fraudulent claims, they’re less likely to raise rates across the board to compensate for those losses. Additionally, predictive analytics can identify potentially fraudulent networks before they cause widespread damage, protecting the insurance pool that covers your properties and personal assets. While no system is perfect, these technological advances represent a significant step forward in protecting honest policyholders from bearing the financial burden of fraud.

The Human Element: Investigators and Special Units

Behind every fraud detection system are dedicated professionals working to protect honest policyholders from inflated premiums. Fraud investigation units employ specialized investigators who analyze billing patterns, conduct interviews, and gather evidence when suspicious claims arise. These teams often include former law enforcement officers and healthcare professionals who understand both medical procedures and criminal tactics.

Medical auditors play an equally crucial role, reviewing thousands of claims to spot anomalies like duplicate billing or services that were never rendered. They use sophisticated data analytics to identify providers whose billing patterns deviate significantly from industry norms.

What makes these efforts truly effective is collaboration. Insurance companies regularly share information with healthcare providers to verify treatments, while law enforcement agencies pursue criminal charges against fraudsters. This multi-layered approach creates accountability at every level. For property owners and real estate professionals, understanding this network matters because successful fraud prevention keeps your insurance costs predictable and protects the integrity of the coverage you depend on for your investments.

Your Action Plan: Protecting Yourself and Your Properties

Document Everything (And Why It Matters)

Think of documentation as your financial shield against fraudulent claims. When incidents occur on your property—whether it’s a slip-and-fall, contractor injury, or tenant accident—immediately photograph everything: the scene, any hazards, weather conditions, and property damage. Time-stamp these photos and store them securely in cloud-based systems.

For medical-related incidents on your property, maintain a contemporaneous log. Record who was present, what happened, witness statements, and any immediate medical attention provided. If someone claims injury weeks later with suspiciously inflated medical bills, your detailed records become invaluable evidence.

Keep organized files of all insurance communications. Save emails, note phone conversation details (date, time, representative name, topics discussed), and retain copies of every form submitted. This paper trail helps identify inconsistencies if fraudulent billing appears later.

Property managers and landlords should require incident reports from tenants within 24 hours of any accident. This creates accountability and makes it harder for dishonest individuals to fabricate or exaggerate claims months down the line.

The documentation habit also protects your premiums. Insurance companies view well-documented properties as lower risk, potentially qualifying you for better rates. More importantly, solid records help you dispute bogus claims quickly, preventing them from appearing on your loss history and driving up future costs.

Vet Your Service Providers and Contractors

Whether you’re a property manager hiring a contractor or a homeowner bringing in service providers, proper vetting is your first line of defense against fraudulent billing schemes. Start by verifying basic credentials: confirm licenses are current and in good standing with your state’s licensing board, and check that their business registration is legitimate. Don’t skip the references—actually call them and ask specific questions about billing practices and claim experiences.

When discussing insurance coverage, ask potential contractors about their workers’ compensation and general liability policies directly. Request certificates of insurance and verify them independently with the insurance carrier, not just the agent. Ask how they handle injury claims and what their claim history looks like over the past three years. A provider who seems evasive about their insurance arrangements or can’t provide documentation quickly might be cutting corners.

For ongoing relationships with property managers or maintenance companies, establish clear billing protocols upfront. Require itemized invoices, not vague lump-sum charges. Specify that any insurance claims must be reported to you within 24 hours. These simple transparency measures make fraudulent billing significantly harder to execute and easier to detect before it impacts your premiums or legal liability.

Review Your Bills Like a Pro

Start by requesting itemized bills for every medical service—yes, every single charge matters. Compare each line item against your insurance Explanation of Benefits (EOB) statement, looking for discrepancies in dates, services you didn’t receive, or duplicate charges. Flag any codes you don’t recognize and research them using free medical billing code databases online.

Next, verify that procedures match what actually happened during your visit. If you underwent a basic consultation but see charges for advanced diagnostics, that’s a red flag. Contact your provider’s billing department directly with specific questions about questionable items. Document every conversation with names, dates, and reference numbers.

When you spot errors or suspected fraud, dispute suspicious charges immediately in writing with both your insurer and medical provider. Request corrections within 30 days and follow up persistently. Keep copies of all correspondence—this paper trail protects you and strengthens your case if escalation becomes necessary.

When to Report Suspected Fraud (And How to Do It Right)

Recognizing when something feels wrong is the first step, but knowing when to actually report it can be trickier. Generally, if you’ve noticed billing patterns that seem deliberately misleading rather than simple clerical errors, it’s time to take action. This includes repeated charges for services never rendered, systematic upcoding across multiple claims, or providers refusing to provide itemized bills when requested.

Start by documenting everything. Keep copies of all bills, explanation of benefits statements, medical records, and any correspondence with providers or insurers. Note dates, amounts, and specific discrepancies. This paper trail becomes crucial evidence.

For property-related injuries covered by homeowners or landlord insurance, contact your insurance company’s fraud hotline first. Most major insurers have dedicated investigative units and take these reports seriously. You’ll typically find the fraud reporting number on your insurer’s website or policy documents.

For broader medical billing fraud, the National Health Care Anti-Fraud Association operates resources at NHCAA.org, while your state’s Department of Insurance handles regional complaints. Each state maintains a fraud bureau with specific reporting procedures. Federal cases involving Medicare or Medicaid should go to the Department of Health and Human Services Office of Inspector General at 800-HHS-TIPS.

Concerned about retaliation? Federal and state whistleblower protections shield individuals who report fraud in good faith. The False Claims Act specifically protects those reporting fraud involving government programs and may even entitle whistleblowers to a percentage of recovered funds. Employees reporting employer fraud have additional protections under various employment laws.

When filing a report, stick to facts rather than assumptions. Describe what you observed, provide documentation, and let investigators draw conclusions. You don’t need absolute proof before reporting; reasonable suspicion based on concrete evidence is sufficient. Insurance fraud drives up premiums for everyone in your community, affecting property insurance costs across the board, making your vigilance valuable for the entire real estate market.

The Ripple Effect: How Fighting Fraud Benefits Everyone

When insurance fraud flourishes unchecked, everyone pays the price—quite literally. Think of fraud prevention as a community effort where your vigilance directly impacts your neighbor’s premiums, and theirs affects yours. Every fraudulent claim that gets paid adds to the industry’s overall costs, which insurers inevitably pass along to policyholders through higher rates. This creates a snowball effect that touches everything from your homeowners insurance to the title insurance costs buyers face when purchasing property.

The mathematics are straightforward but sobering: industry estimates suggest that insurance fraud adds roughly 10% to the average policyholder’s premium. For a homeowner paying $2,000 annually, that’s $200 essentially subsidizing fraudsters. Multiply that across neighborhoods, cities, and entire regions, and you’re looking at billions in unnecessary costs that could otherwise stay in homeowners’ pockets or be invested back into properties.

For real estate professionals, fraud prevention carries additional significance. Property values don’t exist in a vacuum—they’re influenced by the overall cost of homeownership in an area. When insurance premiums skyrocket due to rampant fraud, it affects affordability calculations and can make entire markets less attractive to buyers. Conversely, markets known for insurance integrity tend to maintain more stable, predictable costs that support healthy real estate transactions.

Your role as a real estate professional or informed homeowner extends beyond individual transactions. By understanding how medical billing fraud and other schemes infiltrate the insurance ecosystem, you become part of the solution. Asking informed questions about insurance costs, reporting suspicious activities, and choosing to work with reputable insurance providers creates a culture of accountability. This collective vigilance strengthens the entire marketplace, keeping premiums reasonable, protecting property values, and ensuring that insurance remains a reliable safety net rather than an increasingly expensive burden.

You now have the knowledge and tools to protect yourself against medical billing fraud—and that protection extends far beyond healthcare costs. By staying vigilant about the insurance charges you encounter, whether they appear on medical bills, property insurance premiums, or homeowner’s policies, you’re taking control of your financial future.

The key takeaways are straightforward: regularly review all billing statements, understand what your insurance policies actually cover, question charges that seem inflated or unfamiliar, and report suspicious activity immediately. These simple practices can save you thousands of dollars annually while helping to reduce the broader insurance fraud that drives up costs for everyone in your community.

For real estate professionals and homeowners, this awareness becomes even more critical. Medical billing fraud doesn’t just affect healthcare—it creates a ripple effect that influences property insurance rates, liability coverage costs, and even the overall financial health of real estate markets. When insurance companies lose billions to fraudulent claims, those losses translate into higher premiums across all insurance products, including the policies that protect your most valuable asset: your property.

Moving forward, approach insurance interactions with informed confidence. Whether you’re reviewing a medical bill after a property-related injury, examining your homeowner’s insurance statement, or advising clients on coverage options, remember that fraud prevention starts with individual awareness and action. Your diligence today protects your financial interests tomorrow, ensuring that your real estate investments remain secure and your insurance dollars work for you, not for fraudsters.