A property claim denial or underpayment can cost you thousands of dollars, and the sworn proof of loss form stands as your most powerful legal tool to prevent that outcome. This notarized document serves as your formal, legally binding statement of damages submitted to your insurance carrier, and errors or omissions on this form routinely lead to claim rejections or reduced settlements that leave property owners absorbing losses they’re entitled to recover.

The stakes are particularly high because insurance companies use the sworn proof of loss as the foundation for their investigation and settlement calculations. Once you sign this document under oath, you’re legally certifying the accuracy of every detail—from the date of loss and property description to the precise dollar amount of damages. Any discrepancies between your sworn statement and the insurer’s findings give them grounds to dispute your claim or even deny coverage entirely based on misrepresentation.

Real estate professionals and property owners face this critical juncture during their most vulnerable moments: immediately after suffering fire damage, water intrusion, theft, or natural disaster losses. The insurance company typically requests this form when initial documentation proves insufficient or when claim values exceed certain thresholds, often catching policyholders off-guard during an already stressful recovery period.

Understanding how to complete this form correctly transforms it from a bureaucratic hurdle into a strategic advantage that accelerates your claim resolution and maximizes your recovery amount. The following guidance breaks down exactly what insurers examine, which documentation strengthens your position, and how to avoid the common mistakes that compromise otherwise legitimate claims.

What Exactly Is a Sworn Proof of Loss Form?

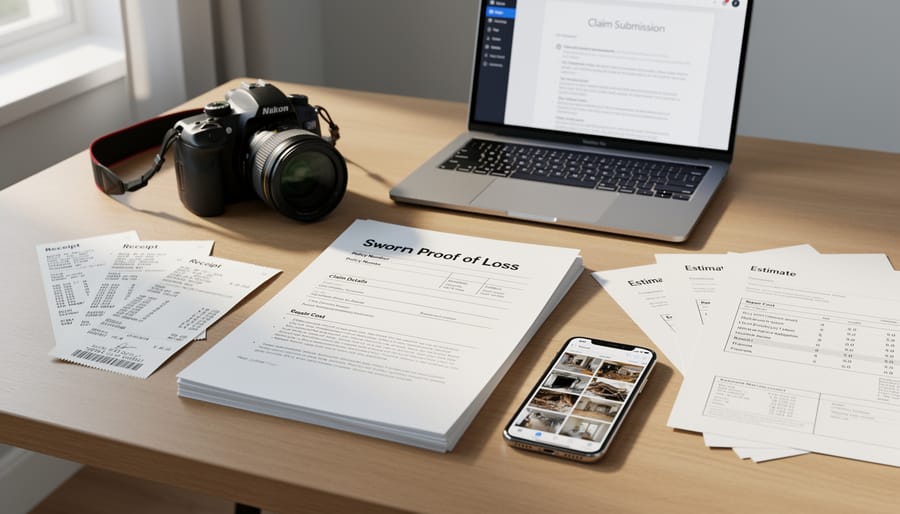

A sworn proof of loss form is a detailed, legally binding document that property owners must submit to their insurance company to formally substantiate their claim for damages or losses. Think of it as the official testimony of what you lost, how much it was worth, and why your insurance policy should cover it. The “sworn” part isn’t just ceremonial—this document requires your signature under oath, typically notarized, making it a legal statement that carries serious consequences if you misrepresent information.

Here’s where it gets important: filing an initial claim and submitting a sworn proof of loss are two distinct steps in the recovery process. When you first report damage to your insurer—whether from fire, water damage, or theft—that’s your initial claim notification. It’s essentially saying, “Something happened, and I need help.” The sworn proof of loss comes later, serving as the comprehensive accounting of your losses that the insurance company uses to determine your settlement amount.

Insurance companies require this documentation for several compelling reasons. First, it protects them against fraudulent claims by requiring you to formally attest to your losses under penalty of perjury. Second, it creates a clear record that both parties can reference during settlement negotiations. Third, most insurance policies actually mandate this form within a specific timeframe—often 60 days after the insurer’s request—making it a contractual obligation rather than a suggestion.

Not every claim requires this level of documentation. Minor claims with straightforward damages may proceed without it. However, for significant property losses, complex damage scenarios, or when claim amounts are disputed, expect your insurer to request this form. Understanding when and why it’s required helps property owners navigate the claims process strategically and avoid unnecessary delays in recovery.

When You’ll Need to File a Sworn Proof of Loss

Most insurance policies require a Sworn Proof of Loss when your claim exceeds a certain dollar threshold, typically ranging from $10,000 to $50,000 depending on your insurer and policy type. This form becomes mandatory in several key scenarios that property owners should understand upfront.

Total loss situations almost always trigger this requirement. If your property sustains catastrophic damage from fire, flooding, or severe weather that renders it uninhabitable or results in a complete structural loss, your insurer will request this formal documentation. Similarly, large-scale damage claims involving multiple systems or significant portions of your property—think roof replacement combined with extensive water damage—typically cross into sworn proof territory.

Some insurers implement this requirement for all theft claims above a modest threshold, while others reserve it for high-value personal property losses. Commercial property claims generally face lower thresholds than residential policies, meaning business owners should expect this documentation more frequently.

Timeline matters significantly here. Most policies stipulate you must submit your Sworn Proof of Loss within 60 to 90 days after your insurer’s request, though this window varies by jurisdiction and policy language. Missing this deadline can jeopardize your entire claim, so mark your calendar immediately upon receiving the request.

Understanding claim processing timelines helps you anticipate when this form might be needed. Your adjuster should communicate requirements clearly during initial assessments, but proactive property owners often inquire about potential documentation needs early in the process to avoid last-minute scrambling when deadlines loom.

Essential Components Every Sworn Proof of Loss Must Include

Policy and Property Information

Getting your policy and property information right on the sworn proof of loss form is non-negotiable. This section requires precise documentation that matches your insurance policy exactly. Start by locating your policy number, which you’ll find on your declarations page or any correspondence from your insurer. Double-check every digit, as even a single mistake can delay your claim significantly.

For property details, include the complete address as it appears on your policy documents. If you own multiple properties under one policy or have separate policies for different units, clarify which specific property the claim addresses. This becomes especially important for real estate investors managing rental portfolios where coverage types may vary by property.

Document all named insureds and additional insureds accurately. In real estate transactions, this might include co-owners, business entities, or mortgage lenders with insurable interests. Review your coverage types carefully, whether it’s replacement cost, actual cash value, or specialized coverage for investment properties. Understanding these distinctions helps you frame your loss claim appropriately and ensures you’re seeking the correct compensation tier your premium supports.

Detailed Loss Description and Documentation

Documenting your property damage thoroughly can mean the difference between a fully paid claim and a disappointing settlement. When describing damage in your sworn proof of loss, specificity is your strongest asset. Don’t simply write “water damage to living room”—instead, detail exactly what was affected: “water damage to 400 square feet of oak hardwood flooring, two leather sofas, entertainment center, and drywall extending four feet up the north and east walls.”

Always include precise dates and times. Note when you first discovered the damage, when the loss-causing event occurred (if different), and when you reported it to your insurer. This timeline establishes credibility and helps adjusters process your claim efficiently.

Photographic evidence is non-negotiable in today’s claims environment. Take wide-angle shots showing the extent of damage, then close-ups capturing specific items and details. Photograph serial numbers, brand labels, and receipts when possible. Videos can be particularly effective for documenting water intrusion or structural issues.

When explaining the cause of loss, be factual and avoid speculation. If a pipe burst caused flooding, describe what you observed without diagnosing why the pipe failed unless you have professional documentation. Insurers appreciate honest, straightforward accounts supported by contractor assessments, weather reports, or incident reports that corroborate your description of events.

Complete Inventory and Valuation

Creating a comprehensive inventory is perhaps the most time-consuming yet critical component of your sworn proof of loss. Start by walking through your property room by room, documenting every damaged or destroyed item with photographs or video. For each item, you’ll need to determine both the replacement cost (what you’d pay today for a new equivalent) and the actual cash value (ACV), which factors in depreciation based on age and condition.

Real estate professionals understand this distinction matters significantly for fixtures and improvements. That upgraded kitchen backsplash or custom-built shelving requires documentation showing original purchase price, installation date, and current replacement estimates. Gather receipts, invoices, contractor quotes, and professional appraisals whenever possible. If original receipts are lost, credit card statements or bank records can serve as backup.

For major improvements like HVAC systems, roofing, or flooring, obtain written estimates from licensed contractors detailing replacement costs. Insurance adjusters appreciate thorough documentation, and detailed appraisals strengthen your position during negotiations. Don’t overlook smaller fixtures like light fixtures, ceiling fans, or built-in appliances—these add up quickly. The more supporting evidence you provide upfront, the smoother your claims process will proceed, reducing back-and-forth delays that extend settlement timelines.

The Sworn Statement and Notarization

When you sign a sworn proof of loss form, you’re doing more than just filling out paperwork—you’re making a legal declaration under oath. This means you’re certifying that all the information you’ve provided is true and accurate to the best of your knowledge. Think of it as testifying in court, but on paper. You’re affirming the details of your loss, the value of damaged property, and any supporting facts related to your claim.

The notarization requirement adds another layer of legal validity to your statement. A notary public, who serves as an impartial witness, verifies your identity and watches you sign the document. This process protects both you and your insurance carrier by ensuring the authenticity of your claim and preventing fraud.

You can get your sworn proof of loss notarized at several convenient locations. Most banks offer free notary services to account holders, while UPS stores and shipping centers typically charge a small fee. Many insurance agents also have notaries on staff or can direct you to one. If you’re working with a public adjuster on your property claim, they often coordinate the notarization as part of their service.

Step-by-Step: Preparing Your Sworn Proof of Loss

Gather Your Documentation Arsenal

Before you tackle the sworn proof of loss form, you’ll need to assemble a comprehensive documentation arsenal. Think of this as building your evidence portfolio—the stronger your documentation, the smoother your claims recovery process.

Start with your insurance policy itself, including all endorsements and declarations pages. Your insurer needs to verify coverage details, so have the complete policy ready. Next, gather photographic or video evidence of the damage. Take multiple angles and include wide shots for context alongside close-ups of specific issues.

Financial documentation is equally critical. Collect original receipts for damaged items, purchase invoices, and records of documenting home improvements that increased property value. For real estate claims, you’ll also need contractor estimates for repairs—get at least two competitive bids to strengthen your position.

Don’t overlook previous property appraisals, which establish baseline values before the loss occurred. If you have a mortgage, include your lender’s information, as they may be listed as a loss payee on your policy. Finally, maintain a detailed inventory list describing each damaged item, its age, condition, and replacement cost. This organized approach demonstrates professionalism and expedites the adjustment process significantly.

Calculate Your Loss Accurately

Accurately calculating your loss is the cornerstone of maximizing your insurance recovery. Start by documenting the replacement cost of damaged items—what it would cost today to replace them with similar quality materials. For real estate improvements like custom cabinetry or upgraded flooring, gather recent invoices, contractor estimates, and comparable market prices to establish baseline values.

Here’s where it gets tricky: insurers will apply depreciation based on the age and condition of damaged property. A ten-year-old roof, for instance, won’t receive full replacement value unless you have guaranteed replacement cost coverage. Understanding this calculation prevents unpleasant surprises during settlement.

For significant property damage exceeding $50,000 or complex commercial real estate claims, hiring a professional appraiser or public adjuster becomes essential. These experts understand local construction costs, proper depreciation schedules, and industry-standard valuation methods that DIY calculations often miss. They’ll document everything from structural damage to lost rental income, ensuring your sworn proof of loss reflects the complete financial impact.

Keep detailed records of all appraisals, estimates, and calculations. Your insurance company will scrutinize these figures, so professional documentation strengthens your position during negotiations and demonstrates the legitimacy of your claimed amounts.

Complete the Form Without Common Errors

Accuracy matters when completing your sworn proof of loss form—mistakes can delay or reduce your settlement. Start by using specific language rather than vague descriptions. Instead of writing “damaged kitchen,” specify “water damage to 200 square feet of hardwood flooring and three lower cabinets.” Include precise measurements, dates, and dollar amounts backed by receipts or professional estimates.

Double-check all calculations before submission. A simple math error can raise red flags with adjusters and slow your claim. Organize your documentation logically, grouping items by room or category to make verification easier.

Be thorough without overwhelming the form with unnecessary details. Stick to facts directly related to the loss. Avoid emotional language or speculation about what caused the damage—that’s the adjuster’s determination.

Review the form multiple times, ideally having another person check it for clarity and completeness. Remember that this sworn document has legal implications, so ensure every statement is accurate and defensible. Understanding insurance payout taxation considerations beforehand helps you approach the claim strategically and avoid unwelcome surprises.

Review, Sign, and Submit Properly

Before submitting your sworn proof of loss form, take time for a thorough final review. Check that all dollar amounts match your supporting documentation, dates are accurate, and every section is complete. Missing information can delay your claim significantly. Verify that property descriptions align with your policy documents and that you’ve included all damaged items with their corresponding values.

Next, obtain proper notarization—this step is non-negotiable. Schedule an appointment with a licensed notary public, bring valid identification, and sign the form in their presence. Many banks offer free notary services to account holders, or you can find mobile notaries for convenience. Remember, signing before reaching the notary invalidates the document.

For submission, follow your insurance company’s specific requirements. Most insurers accept submissions via certified mail, email, or online portal uploads. Certified mail provides proof of delivery and creates a paper trail. If submitting electronically, request confirmation of receipt and note the submission date.

Keep multiple copies for your records—one physical and one digital backup. This documentation protects you if disputes arise and serves as reference material should you face similar claims in future properties. Consider storing copies with other important real estate documents in a secure location separate from the insured property.

Critical Mistakes That Sabotage Claims Recovery

Even experienced property owners make critical errors when completing their sworn proof of loss form, and these mistakes can cost thousands in denied or reduced claims. Understanding what not to do is just as important as knowing the correct procedures.

One of the most damaging errors is undervaluing your losses. Many claimants rush through the itemization process, estimating values from memory rather than conducting thorough research. A real estate investor in Florida lost $47,000 in recovery because she listed replacement costs based on what she originally paid years ago, ignoring current market values and appreciation. Always document current replacement costs with receipts, professional appraisals, or comparable market pricing.

Missing deadlines represents another critical pitfall. Most insurance policies require submission within 60 days of the insurer’s request, though this varies by state and policy. A commercial property owner in Texas had his entire $200,000 claim rejected because he submitted his form three days late, assuming the deadline was flexible. Set calendar reminders and submit early to allow for potential corrections.

Incomplete documentation creates unnecessary delays and raises red flags with adjusters. Submitting a proof of loss without supporting photographs, receipts, contractor estimates, or repair invoices signals disorganization and invites scrutiny. One property manager learned this lesson when her claim stalled for eight months due to missing documentation for tenant improvements.

Inconsistent statements between your initial claim report and your sworn proof of loss form can suggest fraud, even when discrepancies result from honest mistakes. Review all previous communications with your insurer before completing the form to ensure alignment.

Finally, failing to separate personal property from real property damages causes significant complications. These categories have different coverage limits, deductibles, and depreciation schedules. A homeowner who lumped together structural damage with furniture losses faced a $15,000 reduction because the adjuster reclassified everything under the lower personal property limits. Categorize each item correctly from the start.

When to Bring in Professional Help

Knowing when to call in professional assistance can mean the difference between a fair settlement and leaving thousands of dollars on the table. If your claim exceeds $50,000, involves disputed damage assessments, or your insurer denies coverage, it’s time to consider expert help.

Public adjusters work exclusively for you, not the insurance company, and typically charge 5-15% of your settlement. For a $100,000 claim, spending $10,000 to secure an additional $30,000 in recovery makes financial sense. They’re particularly valuable for complex commercial properties, multi-unit buildings, or claims involving specialized damage like foundation issues or environmental hazards.

Property appraisers become essential when there’s disagreement over replacement costs or actual cash value. Their independent assessments carry weight in negotiations and typically cost $500-$2,000, a worthwhile investment when contesting lowball valuations.

Attorneys enter the picture when insurers act in bad faith, delay unreasonably, or when your sworn proof of loss triggers litigation. Most property insurance attorneys work on contingency, taking 25-40% of recovered amounts, so they only get paid if you win.

Red flags that signal professional help is needed include insurers requesting multiple sworn proofs of loss, significant discrepancies between your assessment and theirs, or settlement offers below 50% of your documented losses. Implementing robust claims management strategies from the start can prevent these complications, but don’t hesitate to bring in specialists when stakes are high.

The difference between a successful insurance claim and a disappointing settlement often comes down to preparation and documentation. Your sworn proof of loss form represents more than just paperwork—it’s your financial protection strategy in action. By understanding how to properly complete this critical document, you’re taking control of your claim recovery process and ensuring your real estate investment receives the protection it deserves.

The best time to prepare for filing a claim is before disaster strikes. Start building solid documentation habits today: maintain updated property inventories, keep receipts for major purchases and improvements, photograph your assets regularly, and store copies of important documents in secure, accessible locations. These simple practices will save you countless hours and potentially thousands of dollars when you need to file a claim.

Remember, insurance companies have teams of professionals protecting their interests—you deserve to have the same level of preparedness protecting yours. Whether you’re managing investment properties or safeguarding your personal residence, thorough documentation and understanding the sworn proof of loss process empowers you to navigate claims with confidence and maximize your rightful recovery.