The real estate transaction that once took 60 days now closes in 10. The investment opportunity that required $500,000 now opens at $5,000. The mortgage approval that demanded weeks of paperwork now delivers decisions in hours. This isn’t a glimpse into the future—it’s happening right now, powered by fintech innovations reshaping how we buy, sell, and finance property.

Financial technology has moved beyond disrupting traditional banking to fundamentally transform real estate’s oldest pain points. Blockchain platforms are eliminating title insurance inefficiencies and reducing closing costs by thousands of dollars. Artificial intelligence algorithms assess creditworthiness with nuanced precision that traditional underwriting never achieved, opening homeownership doors for creditworthy buyers previously locked out by rigid FICO score requirements. Digital mortgage platforms compress application-to-approval timelines from weeks to days, while automated valuation models deliver property assessments in minutes rather than waiting for scheduled appraisals.

Perhaps most dramatically, crowdfunding platforms and tokenization are democratizing real estate investment. What was once the exclusive domain of institutional investors and high-net-worth individuals now welcomes everyday investors with fractional ownership opportunities. A software engineer in Austin can own shares in a Miami commercial property. A teacher in Portland can diversify into industrial real estate across multiple markets. The barriers that kept average Americans from building wealth through property investment are crumbling.

These innovations aren’t merely conveniences—they represent fundamental shifts in accessibility, transparency, and efficiency. Michael Bondi, a realtor in Las Vegas, states, “understanding how blockchain, AI, and digital platforms operate within real estate financing isn’t optional knowledge anymore; it’s essential for anyone navigating today’s property markets.” Whether you’re a first-time homebuyer, seasoned investor, or real estate professional, these technologies are already reshaping your opportunities and strategies in ways that demand attention and adaptation.

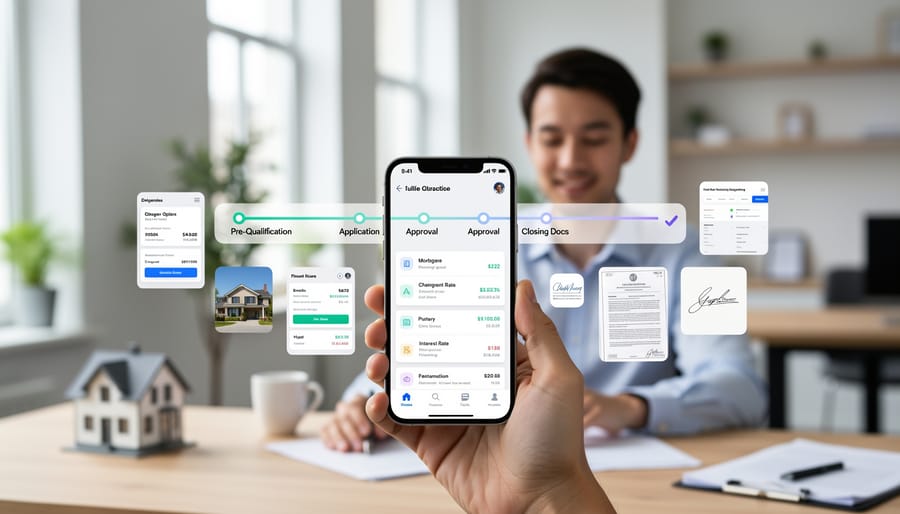

The Digital Mortgage Revolution: From Weeks to Days

Automated Underwriting Systems That Actually Work

Gone are the days of waiting weeks for mortgage approval while your dream home slips away to another buyer. Automated underwriting systems powered by artificial intelligence are revolutionizing how lenders evaluate loan applications, transforming a process that once took 30-45 days into one that can be completed in hours or even minutes.

These AI-driven platforms analyze hundreds of data points simultaneously—from credit scores and employment history to bank statements and property valuations—identifying patterns and risk factors that humans might miss or take days to uncover. The result? More consistent, accurate decisions with significantly fewer errors. Think of it as having a tireless expert who never gets fatigued or distracted, working 24/7 to assess your financial profile.

For borrowers, the benefits are clear: faster decisions mean you can make competitive offers with confidence, knowing your financing is secure. Pre-approval letters carry more weight when backed by sophisticated AI analysis. For lenders, automated underwriting reduces operational costs while maintaining rigorous standards. The technology flags potential issues early, allowing underwriters to focus their expertise on complex cases that truly require human judgment.

What makes modern systems particularly impressive is their ability to consider alternative data—like consistent rent payments or utility bills—which helps borrowers with limited credit history qualify for loans they might have been denied under traditional methods. This isn’t about lowering standards; it’s about making smarter, more inclusive lending decisions based on a complete financial picture rather than outdated formulas.

The End of Paperwork Mountains

Remember the days of drowning in mortgage paperwork? That mountain of documents requiring your signature in triplicate is rapidly becoming history, thanks to fintech innovations transforming how real estate transactions are documented and stored.

Digital document management systems now allow you to sign, share, and store every piece of your property transaction online. These platforms organize everything from purchase agreements to inspection reports in secure cloud environments, accessible anytime from your smartphone or computer. No more frantic searches through filing cabinets or worried calls about whether that crucial document was actually submitted.

E-closing platforms take this convenience further by enabling completely virtual closings. You can finalize your home purchase from your living room, digitally signing documents with legally binding e-signatures. These e-mortgage solutions cut processing times from weeks to days while reducing errors that occur when manually handling dozens of forms.

Perhaps most revolutionary is blockchain-based record keeping, which creates permanent, tamper-proof digital ledgers of property ownership and transaction history. Think of it as a digital chain of custody that tracks every document, payment, and ownership change automatically. This technology eliminates the need for extensive paper trails while providing unprecedented security and transparency.

For homebuyers, these innovations mean faster closings and fewer trips to notary offices. Real estate professionals benefit from streamlined workflows and reduced administrative burden. Most importantly, everyone gains peace of mind knowing their important documents are securely stored and easily retrievable whenever needed.

Crowdfunding Platforms: Making Real Estate Investment Accessible

From $100,000 Minimums to $500 Entry Points

Traditional real estate investment once belonged exclusively to the wealthy. Until recently, if you wanted to invest in commercial properties or participate in large-scale residential developments, you needed six-figure minimums and connections to private investment networks. That landscape has fundamentally changed.

Real estate crowdfunding platforms have shattered these barriers, allowing everyday investors to enter the market with as little as $500. These digital platforms pool capital from multiple investors, enabling fractional ownership in properties that would otherwise remain inaccessible.

This democratization carries significant implications for portfolio diversification. Previously, many investors concentrated their wealth in single properties or traditional stocks and bonds because they lacked the capital for broader real estate exposure. Now, that same investor can spread $5,000 across ten different properties in various markets, sectors, and risk profiles.

The diversification benefits extend beyond simple risk management. Investors gain access to commercial real estate, multifamily developments, and even specialized niches like healthcare facilities or industrial warehouses. This variety was previously reserved for institutional investors and high-net-worth individuals.

For real estate professionals, this shift means encountering more educated, engaged investors who understand market dynamics through their diversified holdings. The barrier to entry has dropped, but the quality of market participation has risen accordingly.

The Technology Behind Fractional Ownership

At its core, fractional ownership in real estate relies on three key technological innovations that make sharing property ownership practical and transparent.

First, tokenization transforms real estate into digital shares. Think of it like breaking a property into puzzle pieces—each piece represents a specific ownership stake. Using blockchain technology, platforms create digital tokens that prove your ownership of a portion of a property. These tokens are recorded on an immutable digital ledger, ensuring your stake is secure and verifiable at all times.

Second, digital share management systems handle the complex tracking of who owns what. Rather than dealing with mountains of paperwork, these platforms maintain real-time records of all fractional owners, their percentage stakes, and transaction histories. This technology allows investors to buy or sell their shares with the same ease as trading stocks, though with property-specific regulations in place.

Third, automated dividend distribution eliminates the headache of collecting rental income. Smart contracts—self-executing programs on the blockchain—automatically calculate each owner’s portion of rental payments based on their ownership percentage and instantly distribute funds to their accounts. No waiting for checks, no manual calculations, and no disputes about who gets what. This automation ensures timely, accurate payments while reducing administrative costs that would traditionally eat into investor returns.

Blockchain and Smart Contracts: Cutting Out the Middlemen

Smart Contracts That Handle Escrow Automatically

Smart contracts are revolutionizing real estate escrow by automating what traditionally required multiple intermediaries and weeks of waiting. These self-executing digital agreements live on blockchain networks and automatically trigger fund releases when specific conditions are met, think of them as sophisticated digital vaults with built-in rule books.

Here’s how they work in practice: when you’re buying a home, the smart contract holds your deposit and only releases funds to the seller once predetermined milestones are verified. These might include title verification, successful home inspection, or mortgage approval. The contract checks these conditions automatically through connected data sources, eliminating the need for constant manual oversight.

The benefits are substantial. Traditional escrow processes often take 30 to 45 days with multiple back-and-forth communications. Smart contracts can reduce this timeline by 40 percent or more while significantly cutting costs associated with escrow agents and administrative overhead. They also minimize disputes since the contract terms are transparent, immutable, and execute exactly as programmed.

For real estate professionals, this technology means fewer transaction bottlenecks and happier clients. Buyers and sellers gain unprecedented transparency, viewing transaction progress in real-time rather than waiting for phone updates. While adoption is still growing, forward-thinking real estate markets are already integrating these solutions into standard closing procedures.

Blockchain-Based Title Management

Property title management has traditionally been a paper-heavy, time-consuming process vulnerable to fraud and human error. Blockchain technology in real estate is changing this landscape by creating permanent, tamper-proof digital records of property ownership and transaction history.

Distributed ledger technology provides an immutable record of every property transfer, lien, and encumbrance. Once information is recorded on the blockchain, it cannot be altered or deleted without leaving a traceable audit trail. This dramatically reduces title fraud risk, which costs homeowners and lenders millions annually through forged documents and identity theft schemes.

Beyond security benefits, blockchain streamlines the title search process. What traditionally takes days or weeks can now happen in minutes, as all relevant property information is instantly accessible and verifiable. This efficiency translates to faster closings, reduced legal fees, and lower title insurance costs.

Several counties across North America are already piloting blockchain-based land registries, demonstrating real-world applications. For homebuyers and real estate investors, this innovation means greater confidence in property transactions and protection against costly title defects that might otherwise surface years after purchase.

AI-Powered Property Valuation and Risk Assessment

Instant Property Valuations That Rival Traditional Appraisals

Gone are the days of waiting weeks for a traditional appraisal. Automated Valuation Models (AVMs) have transformed property valuation into a near-instantaneous process that’s reshaping how we understand real estate worth. These sophisticated algorithms crunch massive datasets in seconds, analyzing comparable sales from your neighborhood, current market trends, and specific property characteristics like square footage, lot size, and recent renovations.

Think of AVMs as having a digital real estate expert who’s memorized every home sale in your area for the past several years. They consider factors traditional appraisers evaluate—bedroom count, location desirability, property condition—but process this information at lightning speed. Major lenders now rely on AVMs for refinancing decisions and home equity lines of credit, dramatically reducing closing timelines.

While AVMs can’t fully replace human appraisers for complex properties or unique situations, their accuracy has improved remarkably. Most provide valuations within 5-10% of traditional appraisals for standard residential properties. For homeowners curious about their property’s current value or investors screening potential purchases, AVMs offer a cost-effective first step that costs nothing compared to $300-500 traditional appraisals. This technology democratizes property valuation, putting powerful insights into everyone’s hands.

Personalized Financing Based on Your Unique Profile

Traditional mortgage underwriting has long relied on rigid criteria like credit scores, income documentation, and employment history. But what if you’re self-employed, a gig worker, or someone rebuilding credit after a life setback? Enter AI-powered risk assessment, which is revolutionizing how lenders evaluate borrower creditworthiness.

Modern fintech platforms now use machine learning algorithms to analyze hundreds of data points beyond your credit score. These systems examine cash flow patterns from bank statements, rent payment history, utility bill consistency, educational background, and even social indicators to build a comprehensive financial profile. For real estate professionals working with non-traditional clients, this means more financing options than ever before.

The result? A freelance graphic designer with irregular income but consistent savings habits might qualify for competitive rates that traditional underwriting would have denied. A recent immigrant with limited U.S. credit history but strong international credentials could access homeownership sooner. These AI systems don’t just say yes or no—they price risk more accurately, potentially offering better rates to applicants who demonstrate financial responsibility through alternative metrics. This holistic approach is expanding the pool of qualified homebuyers while actually reducing lender risk through smarter data analysis.

Alternative Lending Models: Beyond Traditional Banks

Peer-to-Peer Lending Platforms Connecting Borrowers and Investors

Peer-to-peer lending has revolutionized how real estate investors and homebuyers access capital by cutting out traditional financial institutions as middlemen. Peer-to-peer lending platforms use sophisticated algorithms to match borrowers seeking property financing directly with individual or institutional investors looking for attractive returns.

This direct connection creates a win-win scenario. Borrowers often secure funding at more competitive interest rates than conventional bank loans, while investors earn higher returns than typical savings accounts or bonds. The digital infrastructure behind these platforms enables faster approval processes, sometimes delivering decisions within 24-48 hours compared to weeks with traditional lenders.

For real estate transactions, P2P lending has opened doors for investors who might not meet strict bank criteria but have solid property deals and repayment capacity. These platforms assess creditworthiness using alternative data points beyond traditional credit scores, including property value, rental income potential, and borrower experience.

The transparency is another game-changer. Both parties see exactly where their money goes or comes from, with detailed loan terms, risk ratings, and expected returns laid out clearly. This democratization of real estate financing has made property investment more accessible while giving everyday investors opportunities previously reserved for institutional players.

Alternative Credit Scoring: Looking Beyond FICO

Traditional credit scoring models like FICO have long served as gatekeepers to homeownership, but they tell an incomplete story. Nearly 45 million Americans have thin credit files or no credit history at all, effectively shutting them out of conventional mortgage lending despite having solid financial habits.

Enter alternative credit scoring, a fintech innovation that’s reshaping who qualifies for real estate financing. These systems look beyond the Big Three credit bureaus to paint a fuller picture of creditworthiness. Fintech lenders now analyze rent payment history, utility bills, streaming service subscriptions, and even bank account balances to assess borrowing risk.

This approach is particularly transformative for first-time homebuyers, recent immigrants, and younger borrowers who haven’t yet built traditional credit. Companies like Experian Boost and eCredable allow consumers to add positive payment data directly to their credit profiles, potentially boosting scores by 20 points or more.

For real estate professionals, understanding these alternative financing options means serving a broader client base. Progressive lenders are already incorporating alternative data into their underwriting processes, recognizing that someone who consistently pays rent on time likely possesses the discipline needed for mortgage payments. This innovation democratizes homeownership while maintaining responsible lending standards, creating opportunities in previously underserved markets.

Mobile-First Solutions: Real Estate Financing in Your Pocket

Gone are the days of lugging stacks of paperwork to your lender’s office or waiting anxiously by the phone for loan updates. Mobile-first financing platforms have revolutionized how we approach real estate transactions, putting the entire financing journey literally in your pocket.

Today’s mobile financing apps handle everything from initial pre-qualification through final closing, streamlining what was once a frustratingly opaque process. You can snap photos of your pay stubs, upload tax documents, and e-sign disclosures while waiting in line for coffee. These platforms use smart document recognition technology to extract relevant information automatically, eliminating tedious data entry and reducing processing errors.

Real-time status updates represent perhaps the most appreciated feature among borrowers. Instead of playing phone tag with loan officers, you receive instant notifications when your application moves forward, when additional documents are needed, or when underwriting decisions are made. This transparency reduces anxiety and helps you plan your next steps with confidence.

Mobile payment solutions integrated into these apps also simplify financial transactions. From earnest money deposits to closing costs, secure mobile payments eliminate the need for cashier’s checks or wire transfer trips to the bank. You can authorize payments with biometric authentication, adding both convenience and security.

The document management capabilities deserve special mention. Cloud-based storage within these apps means all your financing paperwork stays organized and accessible. Need to reference your appraisal report or review loan terms? Everything’s available instantly, whether you’re at your kitchen table or meeting with your real estate agent.

For professionals, these mobile solutions mean faster deal closures and happier clients. For homebuyers, they represent unprecedented control and visibility into what was historically an intimidating process. The result is a more inclusive, efficient financing ecosystem that serves everyone better.

What These Innovations Mean for You

These fintech innovations aren’t just flashy tech trends—they’re practical tools that can transform how you approach real estate transactions. Here’s how different players in the market can leverage these advancements while avoiding common pitfalls.

For homebuyers, the biggest advantage lies in AI-powered mortgage platforms that can pre-qualify you in minutes rather than weeks. These systems analyze your financial profile instantly, giving you a realistic budget before you start house hunting. However, don’t rely solely on automated approvals. Always review the terms carefully and compare offers from multiple lenders, as algorithms can sometimes miss nuances in your financial situation. Digital closing platforms also mean you can complete transactions remotely, saving time and travel costs—particularly valuable in competitive markets where speed matters.

Real estate investors should explore blockchain-based property platforms and crowdfunding opportunities that weren’t accessible a decade ago. These tools lower entry barriers, allowing you to diversify with smaller capital outlays. You can now invest in commercial properties or development projects that previously required millions in upfront capital. The caution here: thoroughly vet the platform’s track record, understand the liquidity constraints, and never invest more than you can afford to lose. Smart contracts automate many processes, but they’re only as good as their programming—read the fine print before committing funds.

Industry professionals need to embrace these technologies to remain competitive. Familiarize yourself with the major platforms your clients are using, and consider partnering with fintech providers to streamline your operations. Automated underwriting doesn’t replace your expertise—it enhances it by handling routine tasks while you focus on complex deals requiring human judgment.

Stay informed by following fintech news outlets, attending industry conferences, and joining professional networks focused on proptech innovations. The landscape evolves rapidly, and early adopters often gain significant competitive advantages. Set aside time monthly to explore emerging platforms and assess how they might benefit your specific real estate goals.

The fintech revolution in real estate financing isn’t a distant promise—it’s happening right now, transforming how we buy, sell, and invest in property. From blockchain-powered title transfers that complete in hours instead of weeks, to AI algorithms that approve mortgages in minutes, these innovations are reshaping the landscape beneath our feet. Digital lending platforms have democratized access to capital, while tokenization is opening doors to investment opportunities that were once reserved for institutional players with deep pockets.

What makes this moment particularly exciting is the accessibility of these tools. You don’t need to be a tech wizard or a Wall Street insider to benefit from fintech innovations. Whether you’re a first-time homebuyer exploring instant pre-approvals, a real estate professional streamlining closings with smart contracts, or an investor diversifying through crowdfunding platforms, these technologies are ready for you to leverage today.

The key is staying informed and willing to explore new options for your next transaction. Those who embrace these innovations now will find themselves ahead of the curve, enjoying faster processes, lower costs, and greater transparency than traditional methods ever offered.

As we look forward, the evolution shows no signs of slowing. Emerging technologies like decentralized finance and advanced predictive analytics promise even more dramatic shifts ahead. The question isn’t whether fintech will continue transforming real estate financing—it’s how quickly you’ll adapt to harness its full potential.