Florida homeowners face some of the highest homeowners insurance coverage rates in the nation, with average annual premiums exceeding $4,200 – nearly triple the national average. This stark reality stems from Florida’s unique risk profile: frequent hurricanes, intense tropical storms, and widespread flood exposure create a perfect storm for insurance providers. Recent market challenges, including multiple carrier bankruptcies and massive claim increases from severe weather events, have pushed rates even higher. While these costs might seem daunting, understanding the factors driving these premiums is crucial for both current homeowners and prospective buyers in the Sunshine State. Property owners aren’t completely powerless against these high rates – strategic home improvements, careful policy selection, and smart deductible choices can significantly impact premium costs. The key lies in balancing comprehensive protection against Florida’s unique weather risks while implementing proven strategies to maintain affordable coverage.

Why Florida’s Insurance Rates Are Among the Highest

Natural Disaster Risk

Florida’s location and climate make it particularly vulnerable to natural disasters, especially hurricanes and flooding, which significantly impact insurance premiums. The state’s 1,350 miles of coastline exposes properties to severe storm damage, with hurricanes like Ian and Nicole in 2022 causing catastrophic losses for insurance companies.

Insurance providers factor in these risks when calculating premiums, often leading to rates that are 2-3 times higher than the national average. The frequency of severe weather events has increased in recent years, causing insurers to adjust their risk models and raise rates accordingly. Storm surge damage, wind damage, and flooding are particularly costly to insure against.

Many Florida properties require additional coverage beyond standard homeowners insurance, such as separate flood insurance policies, as standard policies typically don’t cover flood damage. The combination of these factors creates a perfect storm for high insurance costs, with some coastal areas seeing annual premiums exceeding $4,000 for average homes. Recent climate change projections suggesting more frequent and intense storms may continue to push these rates higher in coming years.

Insurance Market Instability

Florida’s insurance market is experiencing significant turbulence, with major carriers like State Farm and Allstate drastically reducing their presence or completely withdrawing from the state. This exodus has left many homeowners scrambling to find coverage, often turning to Florida’s insurer of last resort, Citizens Property Insurance Corporation, which now carries over 1.4 million policies.

The instability stems from a perfect storm of challenges: frequent natural disasters, increasing litigation costs, and rampant insurance fraud. Several smaller insurance companies have declared bankruptcy in recent years, leaving policyholders in limbo and further concentrating risk among remaining carriers. This reduced competition has led to sharp premium increases as surviving insurers adjust their rates to accommodate the heightened risk exposure.

Reinsurance costs, which are essentially insurance for insurance companies, have also skyrocketed, forcing carriers to either pass these expenses on to homeowners or exit the market entirely. The situation has created a cycle where fewer options lead to higher prices, making coverage increasingly unaffordable for many Florida residents. Recent legislative reforms aim to stabilize the market, but experts suggest it may take several years before homeowners see significant relief.

Fraud and Litigation Costs

Florida’s insurance market faces significant challenges due to widespread fraud and litigation costs, which directly impact homeowners’ premiums. Assignment of Benefits (AOB) fraud, where contractors convince homeowners to sign over their insurance rights, has led to inflated claims and unnecessary lawsuits. In fact, Florida accounts for nearly 80% of all insurance litigation in the United States despite experiencing only a fraction of the nation’s claims. Roofing scams and fraudulent water damage claims have become particularly prevalent, forcing insurers to increase rates to cover legal expenses and settlement costs. These legal battles and fraudulent activities have contributed to several insurance companies leaving the Florida market entirely, reducing competition and driving up prices for homeowners across the state.

Average Cost Breakdown

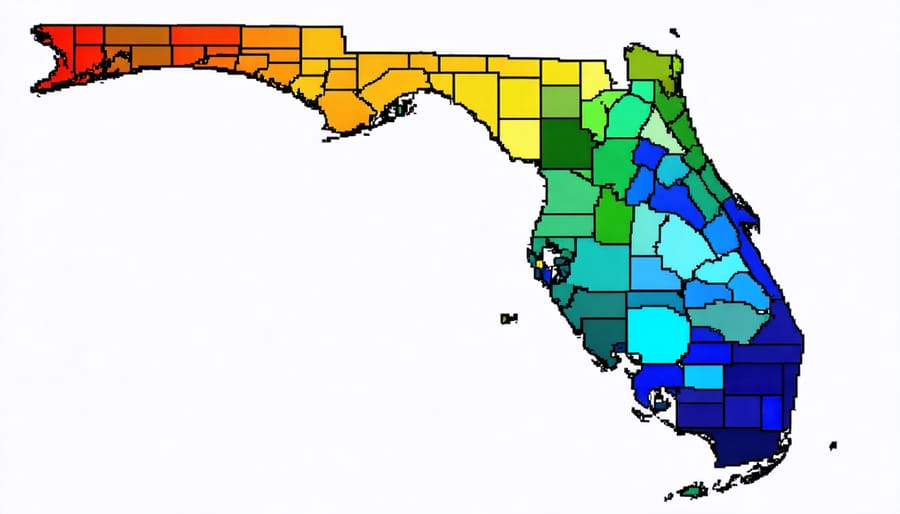

Regional Cost Variations

In Florida, location plays a crucial role in determining homeowners insurance costs, with significant variations between coastal and inland areas. Coastal properties typically face insurance premiums 20-50% higher than similar homes located inland, primarily due to their increased exposure to hurricane risks and storm surge damage.

For example, a standard $300,000 home in Miami-Dade County might have annual premiums ranging from $4,500 to $7,000, while a comparable property in central Florida’s Orlando area might only cost $2,000 to $3,500 to insure. The proximity to coastlines creates this stark difference in pricing.

These regional variations extend beyond just distance from the coast. Properties in South Florida generally face higher premiums than those in North Florida, even when comparing inland areas. This disparity reflects historical storm patterns and population density factors. Additionally, some inland regions near large lakes or rivers may experience higher rates than expected due to flood risks.

Insurance companies use sophisticated mapping tools to assess risk based on exact location, making even a few miles’ difference significant in premium calculations.

Coverage Types and Their Costs

Florida homeowners typically face varying costs depending on their selected essential coverage types. The standard HO-3 policy, which most lenders require, averages $3,500-$4,000 annually for a $250,000 home. This includes dwelling coverage (protecting the structure), personal property protection (15-20% of dwelling coverage), and liability insurance ($100,000-$300,000 range).

Hurricane and flood coverage, crucial in Florida, often require separate policies. Hurricane insurance typically adds $1,500-$2,500 annually, while flood insurance through the National Flood Insurance Program (NFIP) ranges from $600-$2,000 depending on your flood zone.

Additional endorsements like extended replacement cost coverage (adding 10-25% to premiums) or scheduled personal property coverage for high-value items (varying by item value) can further increase costs. Loss assessment coverage for condo owners typically adds $25-$50 annually, while sinkhole coverage might increase premiums by 15-20%.

These costs vary significantly based on location, property value, deductible choices, and insurance provider, making comparison shopping essential for optimal coverage at the best rates.

Smart Ways to Lower Your Premium

Home Hardening Improvements

Making strategic home improvements can significantly reduce your Florida homeowners insurance premiums. Start with fortifying your roof using hurricane-resistant materials and installing impact-resistant windows and doors. These upgrades not only protect your home during storms but can lead to substantial insurance discounts.

Following essential home maintenance tips and implementing wind mitigation features like hurricane straps and reinforced garage doors can qualify you for additional premium reductions. Before starting any modifications, ensure you obtain proper home improvement permits to maintain compliance and maximize insurance benefits.

Consider installing a hurricane-rated secondary water barrier under your roof and reinforcing your gable ends. Many insurance companies offer significant discounts for homes with complete wind mitigation packages, potentially reducing premiums by 20-40%. Smart technology installations, such as water leak detection systems and security monitoring, can also lead to additional savings.

Document all improvements with photos and official inspection reports. Having a certified wind mitigation inspection can help ensure you receive all eligible discounts. Remember to inform your insurance provider about any upgrades, as they won’t automatically apply discounts without proper documentation and notification.

Available Discounts

Florida homeowners can significantly reduce their insurance premiums by taking advantage of various discounts. One of the most substantial savings comes from wind mitigation features, which can lower premiums by up to 45%. Installing impact-resistant windows, hurricane shutters, and reinforced roof-to-wall connections can qualify you for these discounts.

Security system discounts are another valuable option, offering savings between 5-20%. Installing smoke detectors, burglar alarms, and monitored security systems not only protects your home but also reduces insurance costs. Many insurers also offer bundle discounts of 10-15% when you combine your home and auto insurance policies.

New home discounts can save homeowners up to 25%, as newer properties typically have updated electrical, plumbing, and roofing systems. If you’ve recently replaced your roof or upgraded your home’s major systems, you might qualify for modernization discounts ranging from 5-15%.

Other common discounts include:

– Claims-free discounts (5-10% for no claims in 3-5 years)

– Senior citizen discounts (up to 10%)

– Fire sprinkler system discounts (5-10%)

– Gated community discounts (5-20%)

– Early signing discounts (5-10% when renewing early)

Contact multiple insurance providers to compare available discounts, as offerings and qualification requirements vary by company. Remember to document all home improvements and safety features to ensure you receive every eligible discount.

Smart Shopping Strategies

To secure better rates on your Florida homeowners insurance, start by shopping around with multiple insurers. Get at least three to five quotes, and don’t limit yourself to major national carriers – many regional insurers offer competitive rates in Florida. Consider working with an independent insurance agent who can access multiple carriers and understand the local market dynamics.

Bundle your home and auto insurance policies whenever possible, as this typically leads to discounts of 10-25%. Install hurricane-resistant features like impact windows, reinforced doors, and a certified roof system – these improvements can qualify you for significant premium reductions and wind mitigation credits.

Optimize your deductible strategy by choosing a higher hurricane deductible while maintaining a lower all-other-perils deductible. This approach can lower your premium while keeping coverage affordable for non-hurricane claims. Consider maintaining a good credit score, as many insurers use credit-based insurance scores in their pricing.

Review your coverage annually and adjust as needed. Don’t over-insure by including land value in your dwelling coverage, but ensure you have adequate protection for current construction costs. Take advantage of safety discounts by installing security systems, water leak detection devices, and smart home monitoring systems.

Finally, consider establishing a relationship with your insurer through early policy purchase and maintaining continuous coverage, as some companies offer loyalty discounts to long-term customers.

Florida homeowners insurance presents unique challenges due to the state’s distinctive risk factors, but understanding these challenges is the first step toward managing your insurance costs effectively. As we’ve explored throughout this article, several key factors contribute to Florida’s higher insurance rates, including frequent natural disasters, fraud incidents, and litigation costs.

However, homeowners aren’t powerless against these high costs. By implementing multiple mitigation strategies – from installing impact-resistant windows and reinforced roofing to maintaining regular home inspections and documentation – you can significantly reduce your premium costs. Additionally, shopping around for quotes from different insurers, bundling policies, and maintaining a good credit score can lead to substantial savings.

It’s crucial to remember that while Florida’s insurance rates are indeed higher than the national average, the actual cost varies significantly based on factors like location, home value, and construction type. The state average of $3,000 to $6,000 annually serves as a general benchmark, but your specific situation may differ considerably.

For those considering homeownership in Florida or current homeowners looking to optimize their insurance costs, we recommend:

1. Working with a reputable insurance agent who understands Florida’s unique market

2. Investing in home hardening improvements that qualify for insurance discounts

3. Regularly reviewing and updating your policy to ensure appropriate coverage

4. Maintaining detailed records of home improvements and regular maintenance

5. Consider setting aside funds for a higher deductible to lower monthly premiums

While Florida’s homeowners insurance market presents challenges, staying informed and proactive about risk management can help make these costs more manageable. Remember that the right combination of preventive measures, policy choices, and insurance strategy can help you protect your home while keeping costs as reasonable as possible in Florida’s dynamic insurance landscape.