Peer-to-peer lending has emerged as a revolutionary investment vehicle that’s transforming property investment landscapes across North America. With average returns ranging from 7-12% annually, significantly outperforming traditional savings accounts and many conventional investment options, P2P lending demands serious consideration from today’s sophisticated investors.

Yet beneath these attractive returns lies a complex ecosystem of risk and opportunity. While some investors have built robust portfolios yielding consistent passive income through P2P platforms, others have faced substantial losses due to borrower defaults and market volatility. The key distinction often comes down to understanding not just the potential rewards, but also the intricate mechanics of how P2P lending actually works.

This comprehensive analysis will dive deep into the realities of P2P lending as an investment vehicle – examining everything from risk assessment strategies and platform selection to portfolio diversification techniques that can help maximize returns while minimizing exposure. Whether you’re an experienced investor looking to diversify or a newcomer exploring alternative investment options, understanding these fundamentals is crucial for making informed decisions in the evolving P2P lending landscape.

How P2P Real Estate Lending Actually Works

The Platform’s Role

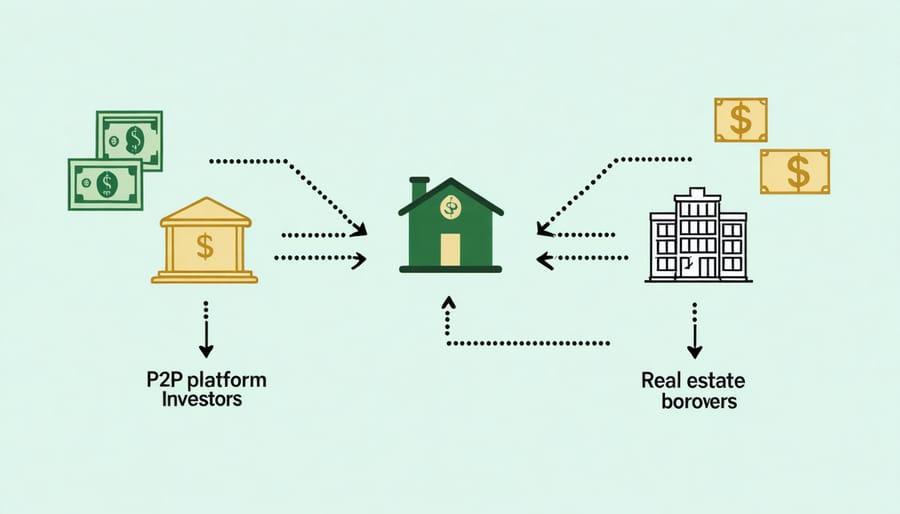

P2P lending platforms serve as sophisticated intermediaries, creating a streamlined marketplace where borrowers and lenders can connect efficiently. These digital platforms handle the critical aspects of loan origination, including borrower screening, credit assessment, and documentation processing.

When a borrower applies for a loan, the platform conducts thorough due diligence, evaluating their creditworthiness through various metrics such as credit scores, income verification, and debt-to-income ratios. Based on this assessment, borrowers are assigned risk grades that determine their interest rates.

For investors, platforms provide detailed loan listings with essential information about borrowers’ profiles, loan purposes, and risk ratings. Most platforms offer automated investing tools that allow lenders to diversify their investments across multiple loans based on predetermined criteria.

The platform also manages all aspects of loan servicing, including payment processing, late payment collections, and default management. They typically charge service fees to both borrowers and lenders, usually a percentage of the loan amount or ongoing management fees.

This infrastructure provides a secure and regulated environment for P2P transactions, making it easier for both parties to participate in direct lending while minimizing operational complexities.

Investment Process

Getting started with P2P lending involves a straightforward but careful process. First, research and select a reputable P2P lending platform that aligns with your investment goals. Popular platforms like Prosper and LendingClub offer different investment options and minimum requirements.

Once you’ve chosen a platform, you’ll need to create an account and complete the verification process, which typically includes providing identification and linking your bank account. Most platforms require a minimum initial investment ranging from $500 to $1,000.

Next, determine your investment strategy. You can either manually select individual loans to invest in or use automated investing tools that allocate your funds based on your predetermined criteria. Many investors start with automated investing to diversify across multiple loans.

Set your risk parameters by choosing loan grades. Higher-grade loans offer lower returns but greater security, while lower-grade loans provide higher potential returns with increased risk. Consider starting with a mix of loan grades to balance your portfolio.

Finally, monitor your investments regularly through the platform’s dashboard and reinvest returns to compound your earnings. Most platforms provide detailed performance metrics and tax documents for your records.

Potential Returns vs Traditional Investments

Expected Returns

P2P lending returns typically range from 7% to 12% annually, though some platforms report returns as high as 15% for well-diversified portfolios. These yields can help investors maximize real estate ROI when compared to traditional investment vehicles like savings accounts or bonds.

Several factors influence your potential returns in P2P lending. Credit grades of borrowers play a crucial role, with higher-risk loans offering higher interest rates but increased default risk. Loan duration also affects yields, with longer-term loans generally providing better rates than short-term options.

Platform fees impact your net returns, typically ranging from 0.5% to 2% of the loan amount. Some platforms charge additional servicing fees or collection fees for defaulted loans. Geographic location and local real estate market conditions can also affect returns, particularly for property-backed P2P loans.

To optimize returns, successful investors often employ diversification strategies across multiple loans, borrower types, and risk grades. Historical data shows that investors who spread their capital across 100+ loans tend to achieve more stable returns and better protection against defaults.

Cost Comparison

When comparing P2P lending with traditional financing options, the cost structures reveal significant differences. P2P platforms typically charge origination fees ranging from 1% to 5% of the loan amount, while traditional banks may charge similar origination fees plus various hidden costs and processing fees.

The overhead costs in P2P lending are notably lower because these platforms operate entirely online, eliminating the need for physical branches and large staff numbers. This cost efficiency often translates to better interest rates for investors, commonly ranging from 6% to 12% annually, compared to the 2% to 4% typically offered by traditional savings accounts or CDs.

However, investors should consider the platform fees, which usually range from 0.5% to 1% of your investment annually. Some platforms also charge servicing fees for managing loan payments and collections. While these fees might seem substantial, they’re generally lower than management fees charged by mutual funds or traditional investment advisors, which can range from 1% to 2% annually.

For real estate-focused P2P lending, the cost advantage becomes more apparent when considering the streamlined process and reduced documentation requirements compared to traditional mortgage lending, potentially leading to faster returns on investment.

Risk Assessment

Default Risk

One of the most significant challenges in P2P lending is managing default risk – the possibility that borrowers may fail to repay their loans. While platforms implement various safety considerations for P2P lending, defaults remain a real concern for investors.

Statistics show that default rates in P2P lending typically range from 3% to 8%, though these figures can fluctuate based on economic conditions and platform-specific factors. During economic downturns, default rates tend to increase, potentially affecting your investment returns.

To mitigate default risk, most P2P platforms employ strict borrower verification processes and credit scoring systems. However, investors should still consider:

– Diversifying across multiple loans to spread risk

– Focusing on higher-grade borrowers, even though they offer lower interest rates

– Understanding the platform’s collection procedures

– Reviewing historical default data for different loan categories

– Maintaining a balanced portfolio with both secured and unsecured loans

It’s worth noting that some P2P platforms offer protection funds or insurance schemes to partially cover losses from defaults. However, these shouldn’t be solely relied upon, as they may have limitations and conditions. Smart investors typically account for potential defaults in their return calculations and maintain adequate reserves to absorb possible losses.

Platform Risk

When considering P2P lending investments, platform risk stands out as a crucial factor that demands careful attention. The stability and longevity of P2P platforms directly impact your investment security, making it essential to understand the regulatory framework for P2P lending in your jurisdiction.

Platform risks manifest in several ways. First, there’s the possibility of platform failure or bankruptcy, which could jeopardize your investments or make loan recovery challenging. While most platforms maintain separate investor accounts, the process of retrieving funds during platform dissolution can be complex and time-consuming.

Additionally, cybersecurity threats pose significant concerns. P2P platforms handle sensitive financial data and facilitate substantial monetary transactions, making them potential targets for cyber attacks. Investors should evaluate a platform’s security measures, including their data protection protocols and insurance coverage against cyber threats.

Regulatory changes can also impact platform operations. As the P2P lending industry evolves, new regulations may affect how platforms operate, potentially altering their business models or investment offerings. Some platforms might struggle to adapt to stricter regulatory requirements, leading to operational challenges or market exits.

To mitigate platform risk, consider diversifying across multiple established platforms, thoroughly reviewing their financial stability, and ensuring they maintain transparent communication about their operations and risk management strategies.

Risk Mitigation Strategies

Portfolio Diversification

One of the most effective ways to manage risk in peer-to-peer lending is through strategic portfolio diversification. Instead of putting all your capital into one or two large loans, spread your investment across multiple smaller loans. For example, if you have $10,000 to invest, consider dividing it into 20 different loans of $500 each.

Most P2P platforms recommend investing in at least 100 different loans to achieve optimal diversification. This approach helps protect your investment if some borrowers default, as the impact on your overall portfolio will be minimal. Think of it as not putting all your eggs in one basket.

Consider diversifying across different:

– Loan grades (from A to D ratings)

– Property types (residential, commercial, mixed-use)

– Geographic locations

– Loan terms (short-term vs. long-term)

– Interest rate ranges

Many P2P platforms offer auto-invest features that automatically spread your investment across multiple loans based on your risk preferences. This tool can save time while maintaining a well-balanced portfolio. Remember to regularly review and rebalance your portfolio as loans are repaid or new opportunities arise.

Due Diligence

Before diving into peer-to-peer lending investments, thorough due diligence is essential to protect your capital and maximize returns. Start by examining the lending platform’s track record, including their default rates, historical returns, and time in business. Look for platforms that are properly registered with regulatory authorities and have transparent reporting practices.

Review the platform’s loan underwriting criteria and risk assessment methods. Understanding how they evaluate borrowers and assign risk grades will help you make informed investment decisions. Pay attention to the platform’s collection procedures and what happens if a borrower defaults.

Diversification is crucial – spread your investments across multiple loans with different risk grades, loan terms, and borrower types. Consider starting with a small amount to test the platform and understand its processes.

Examine fee structures carefully, including origination fees, service charges, and any early withdrawal penalties. Compare these costs across different platforms to ensure you’re getting competitive rates.

Finally, assess your own risk tolerance and investment timeline. P2P lending typically requires a longer-term commitment, so ensure it aligns with your financial goals and liquidity needs.

Real World Performance Data

Looking at real-world performance data from major P2P lending platforms over the past decade reveals both promising returns and notable risks. Historical data from leading platforms shows average annual returns ranging from 5% to 10% for real estate-backed P2P loans, with some investors reporting returns as high as 12-14% on carefully selected opportunities.

However, these figures tell only part of the story. Default rates typically hover between 3% and 7%, though they spiked to nearly 12% during economic downturns. The COVID-19 pandemic particularly highlighted the vulnerability of P2P lending, with some platforms experiencing default rates reaching 15-20% in 2020.

Successful investors often report building diversified portfolios across multiple properties and borrowers. Data shows that investors who spread their capital across at least 100 different loans experienced more stable returns and lower default impacts. The average loan duration ranges from 12 to 36 months, with short-term bridge loans showing slightly higher returns but also increased risk.

Platform-specific performance varies significantly. For instance, larger platforms with stringent vetting processes show default rates around 3-4%, while smaller platforms might see rates twice as high. Geographic location also plays a crucial role, with urban markets typically showing lower default rates than rural areas.

It’s worth noting that these figures reflect pre-fee returns. After accounting for platform fees (typically 1-2%) and potential servicing costs, net returns generally fall 1-3 percentage points below the quoted rates. Despite these considerations, when compared to traditional fixed-income investments, P2P lending continues to offer competitive returns for investors willing to accept the associated risks.

Peer-to-peer lending can be a valuable addition to a diversified investment portfolio, particularly for real estate professionals and investors seeking alternative income streams. While the potential returns of 6-12% are attractive, it’s crucial to approach P2P lending with a well-thought-out strategy and clear understanding of the risks involved.

Success in P2P lending requires careful due diligence, diversification across multiple loans, and a long-term perspective. Start by investing small amounts across different platforms and borrower profiles to minimize risk. Consider allocating no more than 10-15% of your investment portfolio to P2P lending, especially when first entering this market.

For optimal results, focus on platforms specializing in real estate-backed loans, as these typically offer better security through property collateral. Implement a systematic approach by:

– Starting with established P2P platforms with proven track records

– Diversifying across multiple loans (at least 20-30 different investments)

– Setting clear investment criteria based on loan grades and risk tolerance

– Maintaining detailed records of investments and returns

– Regularly reviewing platform performance and loan status

Remember that while P2P lending can offer attractive returns, it should complement rather than replace traditional investment vehicles. By maintaining a balanced approach and understanding both the opportunities and limitations, P2P lending can become a valuable component of your investment strategy.